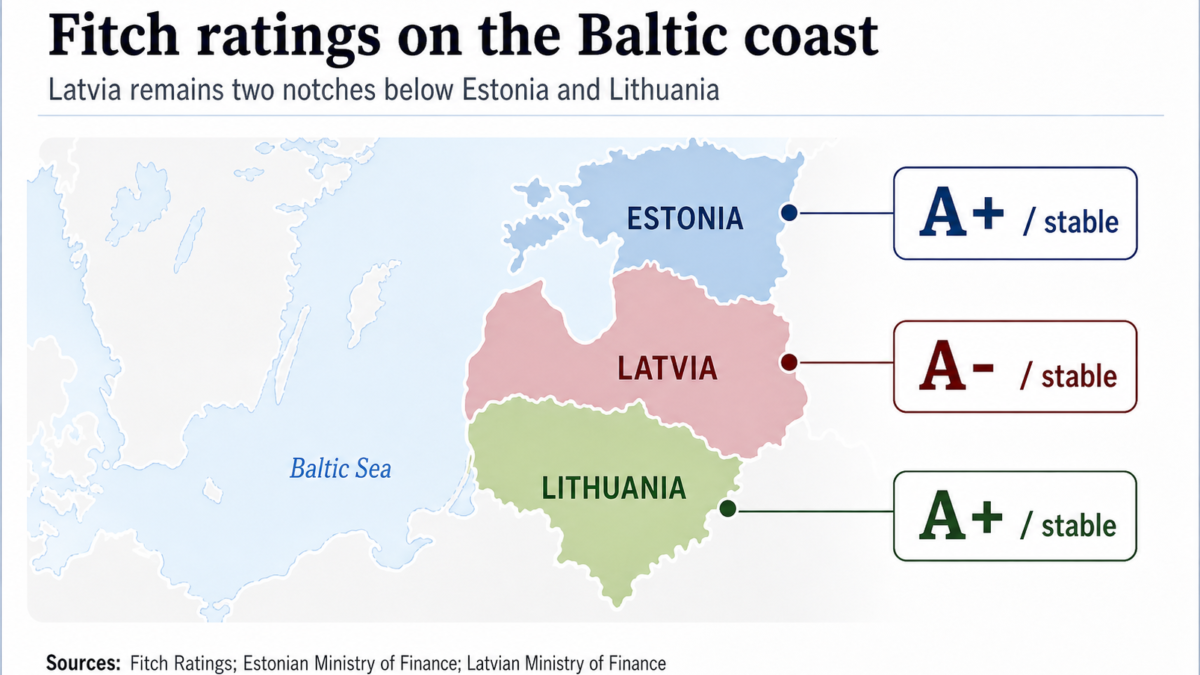

In late April, Latvia and Lithuania received almost simultaneous sovereign rating decisions from Fitch Ratings. Latvia was affirmed at A- with a stable outlook, while Lithuania was upgraded to A+. Estonia, whose A+ rating had been affirmed earlier, remains in the same higher Fitch tier.

Fitch Ratings’ late-April decisions changed the way Latvia’s sovereign rating should be read in a Baltic context. Latvia’s long-term foreign-currency issuer default rating was affirmed at A- / stable on 24 April 2026. On the same day, Lithuania moved up to A+ / stable. Estonia had already been confirmed in that same higher tier on 5 December 2025, according to Estonia’s Ministry of Finance. (fitchratings.com)

As a result, Fitch’s current Baltic sovereign rating map looks as follows:

Data card: Fitch sovereign ratings in the Baltics

| Country | Fitch rating | Latest Fitch action | Date |

|---|---|---|---|

| Estonia | A+ / stable | Affirmed | 5 Dec 2025 |

| Lithuania | A+ / stable | Upgraded from A to A+ | 24 Apr 2026 |

| Latvia | A- / stable | Affirmed | 24 Apr 2026 |

Estonia and Lithuania are currently rated A+ / stable by Fitch. Latvia is rated A- / stable. Estonia’s rating was affirmed slightly earlier despite a difficult economic cycle, while Lithuania’s upgrade came on the same day as Latvia’s affirmation. The comparison puts Latvia two Fitch notches below both Baltic neighbours. (fin.ee)

A strong rating — but not the Baltic top tier

An A- rating is not a weak rating. It places Latvia firmly inside the investment-grade A category and reflects continued confidence in the country’s institutional framework, EU and eurozone membership, and ability to manage public finances. Fitch’s April assessment points to Latvia’s credible policy framework, moderate government debt compared with peers, and relatively low debt-servicing costs. (fitchratings.com)

The question is different: why has Latvia not moved higher?

Latvia has held Fitch’s A- rating since June 2014, when the agency upgraded the country from BBB+ to A- after the post-crisis recovery and Latvia’s entry into the euro area. Since then, the rating has become a long-running threshold rather than a step towards the next tier. (fitchratings.com)

This is why A- looks like a glass ceiling. It is a good rating. It is not a downgrade. But in the Baltic comparison, it has become a visible limit: Estonia has kept A+ despite a weak economic cycle, Lithuania has just moved up to A+, and Latvia remains where it has been since 2014 — credible, stable, investment-grade, but still below its neighbours.

What Fitch sees as Latvia’s constraints

Fitch’s Latvia assessment is not a political judgement. It is a creditor’s view of the country’s risk profile. The agency continues to recognise Latvia’s institutional strengths, but it also points to the structural factors that hold the rating back.

The first constraint is scale. Latvia is a small economy, and that makes it more exposed to external shocks than larger and more diversified peers. The second is income level: Latvia’s GDP per capita remains lower than that of stronger A-rated sovereigns. The third is external balance: Fitch continues to mention external imbalances as one of the weaknesses in Latvia’s rating profile. (fitchratings.com)

The fiscal picture is also becoming more demanding. Defence spending is rising sharply. Fitch notes that Latvia’s core defence spending target is set to rise to 5% of GDP from 2027, with spending projected at 4.7% of GDP in 2026, compared with an estimated 3.7% in 2025. Higher defence expenditure may be strategically necessary, but it narrows fiscal space and makes the medium-term budget path more difficult. (fitchratings.com)

Growth is expected to recover, but its composition matters. Fitch projects Latvia’s GDP growth at 2.3% in 2026 and 2.6% in 2027, with public investment playing a key role. In practical terms, this means that state-led and EU-funded capital spending — infrastructure, defence, energy, municipal projects and other public investment flows — is doing much of the work. That supports GDP, but it is not the same as a broad-based private investment cycle. (fm.gov.lv)

What Fitch is effectively telling Latvia

Fitch does not write an economic reform programme for the Latvian government. But its rating drivers show what would need to change for the country to move above A-.

| Fitch signal | What it means for Latvia |

|---|---|

| Small economy and lower GDP per capita constrain the rating | Latvia needs stronger income convergence, productivity growth and a deeper private-sector base. |

| External imbalances remain a weakness | The economy needs a broader export base, stronger services exports and less vulnerability to external shocks. |

| Growth is supported largely by public investment | Public and EU-funded capital spending helps GDP, but Latvia needs stronger private investment-led growth. |

| Defence spending is rising sharply | Latvia needs a credible fiscal path showing that higher defence costs will not destabilise deficit and debt dynamics. |

| Geopolitical exposure remains a rating constraint | Latvia cannot change geography, but it can reduce economic vulnerability through energy security, infrastructure resilience and diversified trade links. |

| EU and eurozone membership support the rating | Institutional credibility is already a strength. The missing part is broader economic depth. |

The message is not that Latvia lacks fiscal credibility. On the contrary, credibility is what keeps the country in the A category. The issue is that credibility alone has not been enough to push Latvia into the stronger Baltic rating tier.

What could break the A- ceiling?

Breaking the A- ceiling would require more than maintaining fiscal discipline. Latvia already has that reputation. The harder task is to show that the economy has become broader, richer and less dependent on public investment cycles.

The first condition is stronger private-sector-led growth. Latvia would need to show sustained productivity gains, higher private investment, a deeper business sector and stronger export capacity.

The second is faster income convergence. A higher rating would require evidence that Latvia is not only stable, but also moving closer to stronger A-rated peers in income levels, productivity and economic complexity.

The third is a credible fiscal path after the defence spending increase. Defence outlays are likely to remain high, so the rating question is whether Latvia can absorb them without allowing deficits and debt to drift upwards.

The fourth is stronger external resilience. A broader export base, more competitive services, higher value-added production and diversified trade links would help reduce the vulnerability that Fitch continues to identify.

The real issue

Since the financial crisis, Latvia has often treated sovereign ratings as external verdicts: a confirmation is welcomed, a downgrade is feared, and a stable outlook is read as reassurance.

But rating reports are also diagnostic documents. They show what external creditors believe limits a country’s economic strength.

In Latvia’s case, the diagnosis is consistent. The country is credible, disciplined and institutionally anchored in the EU and eurozone. But it remains small, less wealthy than stronger A-rated peers, exposed to geopolitical and external risks, and increasingly constrained by defence-related fiscal pressure.

Latvia has not lost market confidence. But it has not yet built the economic depth needed to move from A- into the Baltic top tier.

The A- ceiling is therefore not only a rating story. It is a development story.