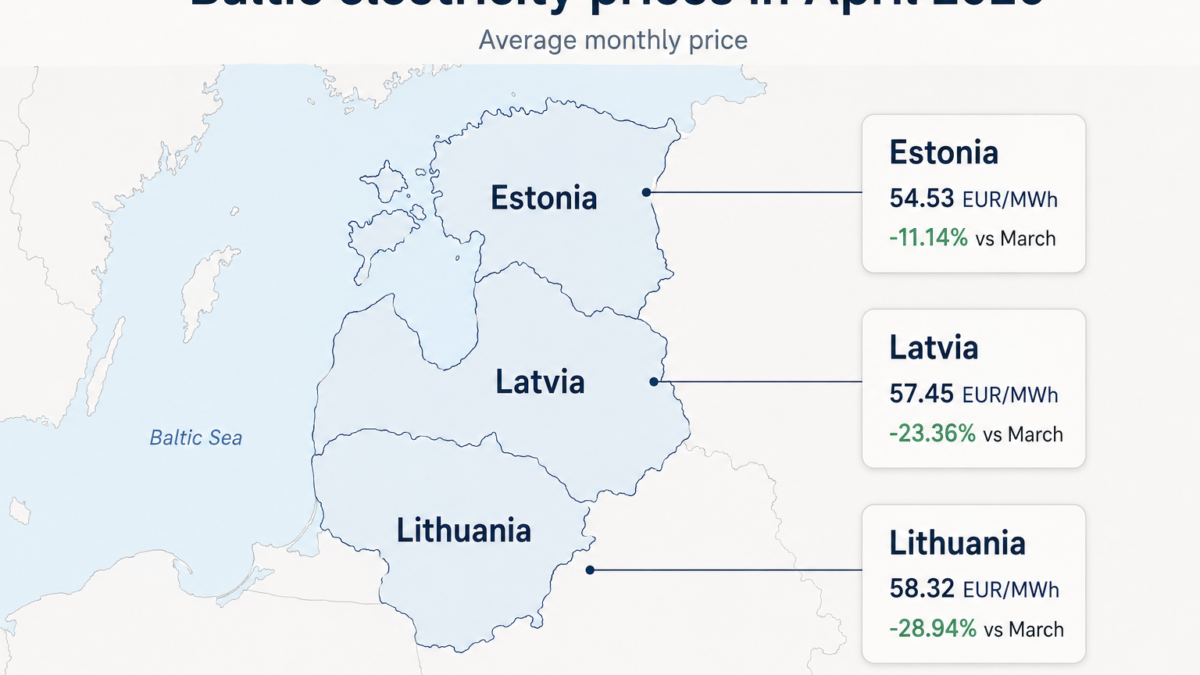

In April 2026, electricity prices continued to fall across the Baltic region. The average price in the Baltic bidding areas declined to 56.77 EUR/MWh, down 22.02% from March and 25.16% lower than in April 2025, according to Latvia’s transmission system operator AS Augstsprieguma tīkls (AST).

The decline was regional, but not identical. Lithuania saw the sharpest monthly fall: −28.94%, to 58.32 EUR/MWh. Latvia’s average price declined by 23.36%, to 57.45 EUR/MWh, while Estonia recorded the lowest price level among the three Baltic states — 54.53 EUR/MWh, down 11.14% from March.

But the April data is important not only because prices fell. It shows how the structure of the Baltic electricity market changes in the warmer season. Lithuanian wind generation, Latvian hydropower and rapidly growing solar generation are starting to push more expensive fossil-based generation almost out of the market. This reduces the need for electricity imports and gives the region a softer energy corridor ahead of the next heating season.

Data card: April 2026

| Indicator | April 2026 |

|---|---|

| Average Baltic electricity price | 56.77 EUR/MWh |

| Change from March | −22.02% |

| Change from April 2025 | −25.16% |

| Latvia | 57.45 EUR/MWh |

| Lithuania | 58.32 EUR/MWh |

| Estonia | 54.53 EUR/MWh |

| Poland | 83.08 EUR/MWh |

| Finland | 49.49 EUR/MWh |

| Negative 15-minute price intervals in Latvia | 84 |

| Negative 15-minute price intervals in Lithuania | 88 |

| Negative 15-minute price intervals in Estonia | 32 |

| Baltic electricity imports from EU countries vs March | −30.4% |

Electricity prices are falling while fuel remains an external risk

The fall in electricity prices contrasts sharply with the situation on the fuel market. In electricity, the Baltic region received support in April from its own seasonal generation base: Lithuanian wind, Latvian hydropower and expanding solar capacity. On the fuel market, there is no comparable domestic cushion. Prices for petrol, diesel and aviation fuel remain much more exposed to external oil prices, logistics, tax burdens and geopolitical risks.

This is why April electricity prices matter as one of the few price stabilisers for the region. They do not remove the broader pressure on transport, freight, aviation and household costs. But they can partially ease the burden on households and businesses, especially for consumers linked to exchange-based or flexible electricity tariffs.

Against this background, the differences between Latvia, Lithuania and Estonia become especially important. The price decline was regional, but each country’s source of resilience was different.

Latvia: cheaper electricity, but hydropower needs watching

In Latvia, the average electricity price in April was 57.45 EUR/MWh. This was 23.36% lower than in March and 26% lower than in April 2025. AST noted that this was already the second consecutive month of decline and the lowest Latvian price level since July 2025.

For Latvia, hydropower remains the key seasonal factor. In spring, the Daugava hydropower cascade traditionally provides an important contribution to the electricity system. Strong hydropower output helps reduce the need for more expensive generation and supports lower prices.

However, this factor needs careful treatment. Hydropower is a strong resource, but not a fully controllable one. Output from the Daugava hydropower plants depends on water inflow, which in turn depends on precipitation and seasonal hydrological conditions.

This means that Latvia’s April position looks positive, but not guaranteed for the whole warm season. The country benefited from the spring hydropower season, but the durability of that support depends on water conditions. If spring inflows weaken faster than usual, or if precipitation is below normal, the contribution of Latvian hydropower may decline. In that case, the role of solar, wind, imports and flexible capacity will increase again.

It is also important to separate price data from the full generation-consumption balance. At the time of AST’s April price review, the detailed Latvian electricity production and consumption balance for April had not yet been published in the monthly balance section. For comparison, in March Latvia produced 765 GWh of electricity while consumption decreased to 666 GWh, meaning domestic generation covered 115% of consumption — the highest level since February 2025.

Lithuania: wind becomes a regional price factor

Lithuania was the structural story of April. According to AST, Lithuania saw the sharpest price decline among the Baltic states, with the average price falling by 28.94% to 58.32 EUR/MWh. Litgrid’s own monthly review gives a rounded movement from 82 EUR/MWh in March to 58 EUR/MWh in April, or a decline of about 29%.

The price change was supported by a major shift in Lithuania’s domestic balance. Litgrid reported that Lithuania’s electricity need in April was 948 GWh, while domestic generation reached 940 GWh. In other words, local generation covered 99% of national electricity need. Lithuania was only 8 GWh short of covering its full monthly electricity need from domestic generation — something that has not happened since the closure of the Ignalina nuclear power plant in 2009.

Wind was the main driver. According to Litgrid, wind farms produced the largest share of Lithuania’s electricity in April. Enefit’s regional overview also shows Lithuania’s growing importance for the whole Baltic market: Lithuania accounted for roughly 78% of Baltic wind generation, while wind and solar generation together were equivalent to around 83% of Lithuania’s electricity consumption.

This is a structural signal. Lithuania is no longer only a large consumer and importer in the regional market. Through wind generation, it is becoming one of the factors shaping the price dynamics of the entire Baltic power system.

In April, Lithuanian wind did not just help Lithuania. It helped define the regional price environment.

Estonia: the lowest price, but a smaller monthly decline

Estonia had the lowest average electricity price among the Baltic states in April — 54.53 EUR/MWh. However, the monthly decline was more moderate than in Latvia or Lithuania: −11.14% from March.

The Estonian market also benefited from milder weather, lower heating demand and stronger solar and wind generation. Enefit noted that April brought the second consecutive monthly fall in Estonian electricity prices, with the average price around 5.4 cents per kilowatt-hour.

The broader regional change was especially visible in fossil-based generation. According to Enefit, Baltic fossil-fuel power plants produced around 1,000 GWh per month in January and February. In April, total fossil-based electricity generation in the region fell to only 120.5 GWh.

For Estonia, this shift matters because the market remains sensitive to dispatchable generation and interconnection availability. When wind, solar and imports work in favour of the system, prices move down. But when winter demand rises and renewable generation is weaker, the region can quickly return to a more expensive configuration.

What April tells us

April does not mean that the Baltic region’s energy risks have disappeared. It shows that those risks are changing shape.

In winter, the region may still lack enough cheap generation. Solar output is lower, wind conditions are variable, electricity consumption rises, and expensive reserve or fossil-based generation becomes more important.

In spring and summer, the picture changes. Cheap domestic generation increases, sometimes so much that electricity prices move into negative territory during specific 15-minute intervals.

In April, there were 84 negative-price intervals in Latvia, 88 in Lithuania and 32 in Estonia. This is not only a market curiosity. It is a signal of insufficient flexibility. The region is becoming better at producing cheap electricity during favourable hours, but it still cannot always store it, shift it or consume it efficiently.

The same can be seen in electricity imports. Total electricity imports into the Baltic states from EU countries continued their downward trend in April and declined by 30.4% from March. Imports from Finland fell by 40%, imports from Poland by 7.3%, while imports from Sweden increased by 5.1%.

Conclusion

The Baltic region has not become energy-secure in a simple or absolute sense. But in 2026 it is entering the summer not as a market fully dependent on external electricity prices, but as a region where domestic renewable generation can soften price pressure, reduce the need for expensive imports and provide more space to prepare for the next heating season.

April showed that Lithuanian wind, Latvian hydropower and growing solar generation across the region are already forming a new seasonal buffer. But this buffer remains weather-dependent. For Latvia, water levels and inflows into the Daugava are crucial. For Lithuania, the key issue is the consistency of wind generation. For Estonia, the main questions are flexible capacity and interconnections.

The next stage of the Baltic energy transition is therefore not only about building more cheap electricity generation. The central question is whether the region can learn to manage surplus electricity in spring and summer as effectively as it tries to cover deficits in winter.