The 2026 spring sowing season in the Baltic states is becoming more than a weather story. Across Latvia, Lithuania and Estonia, farmers are entering the main crop season with a difficult combination: dry topsoil, expensive fertiliser, higher fuel costs and uncertain autumn revenues.

The key question is no longer only how much land will be sown or how much rain will arrive in May. The sharper question is whether the money already put into fields can still translate into yield and margin.

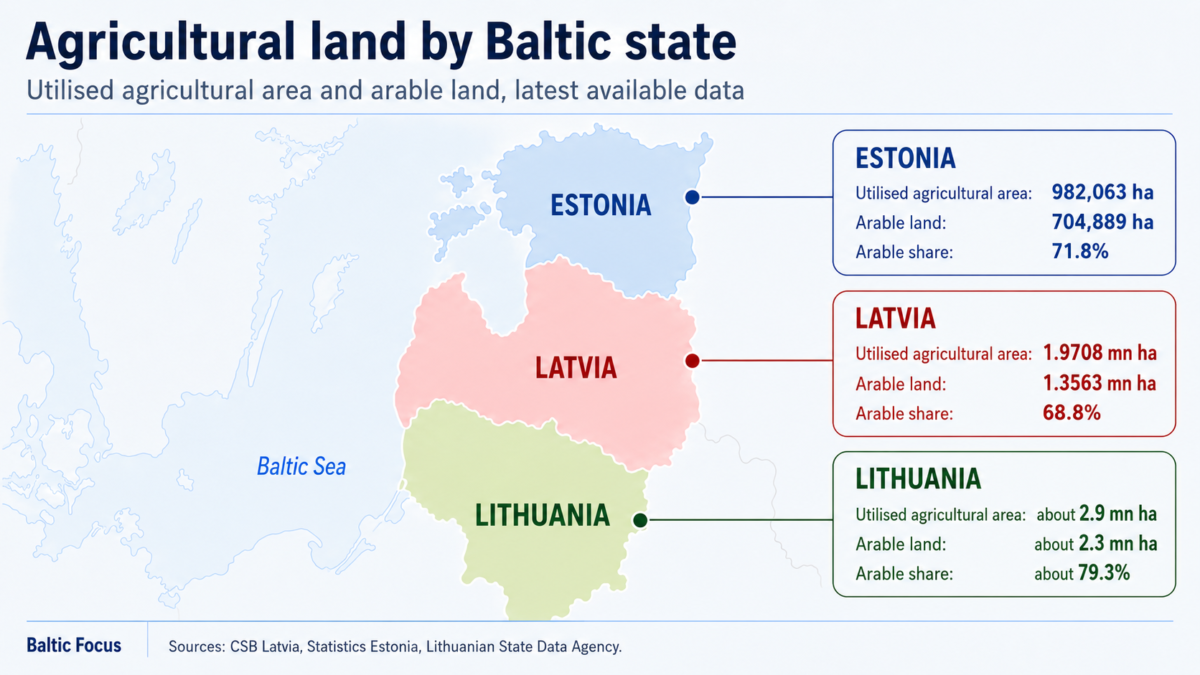

1. The scale of exposure

The scale of exposure is not equal across the region. Lithuania remains the largest agricultural base in the Baltics, with about 2.9 million hectares of utilised agricultural area and around 2.3 million hectares of arable land. Latvia follows with 1.9708 million hectares of utilised agricultural area and 1.3563 million hectares of arable land in 2024. Estonia is smaller in absolute terms, with 982,063 hectares of utilised agricultural area and 704,889 hectares of arable land in 2025.

That means the same weather-and-cost shock has a different weight in each country, even if the underlying pattern is similar.

Data card: Baltic agricultural land exposure

| Country | Utilised agricultural area | Arable land | Reading for 2026 |

|---|---|---|---|

| Lithuania | about 2.9 million ha | about 2.3 million ha | Largest Baltic exposure; dry soil and wind stress matter at the biggest land scale |

| Latvia | 1.9708 million ha | 1.3563 million ha | Mid-sized exposure, with strong grain and rapeseed relevance |

| Estonia | 982,063 ha | 704,889 ha | Smaller land base, but highly consolidated farms and high input-cost sensitivity |

2. Latvia: costs are known, revenues are not

In Latvia, the sowing campaign is already close to completion. Around 90% of fields had been sown by early May, according to estimates cited by Latvian sector representatives. But the sector is still carrying the consequences of the wet autumn of 2025, which delayed harvesting, disrupted autumn sowing and may have reduced the winter rapeseed area by more than 25%.

At the same time, spring 2026 has brought a prolonged moisture deficit, with especially dry conditions in Zemgale and Kurzeme and slower fieldwork in parts of Vidzeme and Latgale.

Latvia’s problem is now clearly economic as well as agronomic. Fuel and fertiliser are the most important cost items, with fuel accounting for around 20% of farm expenses and fertiliser around 30–40%. According to Zemineku Saeima, the price of some nitrogen fertilisers has climbed from about €250 per tonne last autumn to roughly €520 per tonne.

Farmers are responding by shifting their crop structure toward crops that require less mineral fertiliser, including more pulses and oats, while some areas may even be left fallow. In this environment, the main risk is not just lower yield, but the possibility that even a decent harvest may fail to cover the money already invested in the season.

3. Lithuania: dry topsoil becomes a wind-risk problem

Lithuania shows the agronomic side of the same stress with unusual clarity. Field monitoring by Lithuanian agricultural advisers has pointed to very low moisture in the upper soil layer, while wind gusts have been strong enough in some areas to blow away the fertile topsoil.

This matters because a dry spring is not only about a lack of rainfall. Once open fields lose surface moisture, wind becomes a direct production risk, carrying away the very layer in which seed, fertiliser and future yield are concentrated.

Official Lithuanian meteorological data also confirms the difficult background. The national weather service reported local drought during the vegetation period in late April in several municipalities, while dry-period conditions were recorded elsewhere. In parallel, agronomic reports described slow and uneven crop development under cold and dry conditions, with weak nutrient uptake becoming a growing concern.

Lithuania is also where the question of landscape protection becomes easiest to understand. The country has the largest agricultural land base in the Baltics and, in many areas, larger open field blocks. When those fields face dry topsoil and wind pressure, the issue is no longer only drought. It is also exposure.

4. Estonia: May becomes the decision month

Estonia fits the same regional pattern, though the public discussion there is framed more around soil moisture and fertiliser decisions than wind erosion. ERR reported that soil water reserves are at critical levels after a dry and sunny spring. According to Ants-Hannes Viira of the Estonian Chamber of Agriculture and Commerce, the first three months of the year brought only 25–30% of normal precipitation, while April reached only 60% of normal.

In his words, May is the decisive month: if it stays dry, a poor harvest year is likely.

Estonian farmers are already changing their behaviour in the field. One farmer interviewed by ERR said he must think more carefully about whether it makes sense to keep fertilising winter crops if there is not enough moisture for plants to absorb nutrients. He noted that fertiliser prices had risen from about €350 per tonne to €500 per tonne.

Another farmer said he had started rolling spring crops to compact the dry upper layer and preserve the small amount of moisture still left in the soil. This is a strong signal: in Estonia, the spring sowing season is already becoming a financial and operational calculation, not just an agronomic routine.

Prices differ by country, product type and purchase timing, but the direction is the same: nitrogen has become significantly more expensive just as moisture risk has increased.

5. One Baltic pattern, three national expressions

The common denominator is margin pressure, but the channel differs by country. Latvia shows the cost side of the season. Lithuania adds the soil layer: drought is already appearing not only as weak crop development, but also as wind pressure on exposed topsoil. Estonia shows the operational decision point, where farmers must decide whether more fertiliser still makes economic sense without enough moisture.

This is the pattern now emerging across the region: input prices, soil moisture, crop choices and cash flow are no longer separate risks. They are beginning to interact inside the same seasonal calculation.

6. From drainage to soil protection

There is also a deeper structural point here. Baltic agriculture has historically been organised around the opposite problem: too much water. Drainage, field access and the ability to work wet soils have long shaped farm infrastructure. Spring 2026 suggests that this logic may no longer be sufficient on its own.

In a drier and windier spring pattern, farms need not only drainage, but also ways to keep moisture in the field and protect exposed topsoil. The Lithuanian field reports are important here because they describe not only dry soil, but also wind gusts blowing away the fertile upper layer. Once that appears in the field reports, drought is no longer only a water problem. It becomes a soil-protection problem.

The EU policy background also matters. Field margins, tree lines, hedgerows and other landscape features have often been discussed in the CAP context as biodiversity tools or regulatory obligations. But a dry and windy spring gives them another reading. In exposed agricultural landscapes, such elements may also help protect production by slowing wind, retaining moisture and reducing the risk of topsoil loss.

Shelterbelts therefore deserve at least a brief mention. Baltic farmers are being pushed to consider soil-protection tools more often associated with drier, wind-exposed regions. Shelterbelts are one such tool — practical rather than decorative, designed to slow wind, retain moisture and protect fertile topsoil. For Lithuania’s larger open fields, the point is not to copy another model, but to recognise that soil protection may no longer be marginal.

7. A margin test for Baltic agriculture

The immediate risk for 2026 remains straightforward: rainfall in May and early summer will still decide much of the harvest potential. But the broader signal is structural. The issue is no longer only production, but the reliability of the whole seasonal calculation.

That makes the 2026 sowing season a margin test for Baltic agriculture. If rain arrives in time, part of the pressure may ease. If it does not, the region will be left with a harder question: how quickly farms, cooperatives and policy tools can adapt to a spring pattern in which moisture, wind and input costs move against them at the same time.

Postscript

Spring sowing is still progressing daily. By the time this article is published, fieldwork in parts of the Baltic region may be close to completion or already finished. The core issue, however, remains the same: farmers have entered the 2026 season with dry soil, costly inputs and uncertain harvest margins.

Sources used

- Central Statistical Bureau of Latvia, Agriculture of Latvia 2025

- Statistics Estonia, agriculture statistics database

- Lithuanian State Data Agency, agriculture statistics

- Lithuanian Hydrometeorological Service / Meteo.lt

- Lithuanian Agricultural Advisory Service / Agroakademija / IKMIS field monitoring

- ERR / Aktuaalne kaamera reporting on Estonian farmers and spring moisture conditions

- NRA.lv interviews and reporting on Latvia’s 2026 sowing season, Zemnieku Saeima, LATRAPS and sector representatives

- European Commission / CAP / GAEC 8 background on landscape features and non-productive areas