GAZ-SYSTEM has reported another milestone in Poland’s FSRU programme. In May 2026, the vessel for the future terminal in the Gulf of Gdańsk was launched at HD Hyundai Heavy Industries in South Korea. According to the company’s press release, the vessel is expected to arrive in the Gulf of Gdańsk by the end of 2027 and become the core of Poland’s first FSRU terminal.

For Poland, this is part of a wider strategy to strengthen import capacity and its role as a gas hub for Central and Eastern Europe. For the Baltic states, the more important effect is narrower and more commercial: the Gdańsk FSRU strengthens the southern LNG route to a small regional gas market that already has Klaipėda inside the Baltic geography, Inkoo on the northern side and cross-border infrastructure connecting the region to Poland.

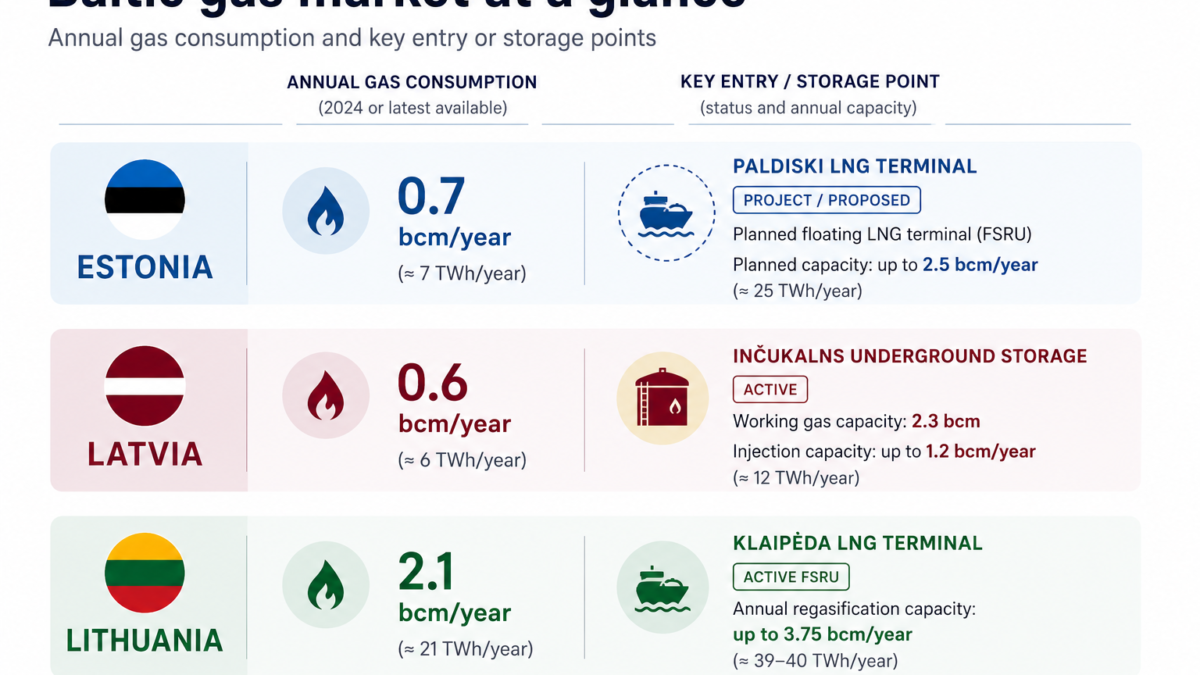

The scale of the market matters. Lithuania consumed 15.9 TWh of gas in 2025. Latvia consumed 8.7 TWh. Estonia’s gas consumption has fallen sharply over the past 15 years; Elering described it at 3.4 TWh in 2023, down from 10 TWh in 2008. Based on the latest available national figures, the three Baltic states represent a gas market of roughly 28 TWh a year. The figure is indicative rather than a single-year statistical total.

Data card: Baltic gas demand is small compared with nearby LNG capacity

| Market / infrastructure | Latest available figure | Comment |

|---|---|---|

| Lithuania gas consumption | 15.9 TWh in 2025 | Down 6.2% from 2024 |

| Latvia gas consumption | 8.7 TWh in 2025 | For Latvian users |

| Estonia gas consumption | 3.4 TWh in 2023 | Down from 10 TWh in 2008 |

| Baltic gas demand, approximate | around 28 TWh/year | Indicative; not a single-year statistical total |

| Klaipėda LNG capacity | about 39–40 TWh/year | 3.75 bcm/year technical capacity |

| Inkoo FSRU capacity | more than 40 TWh/year | 140 GWh/day regasification capacity |

| Świnoujście LNG capacity | about 87 TWh/year | 8.3 bcm/year after expansion |

| Planned Gdańsk FSRU | about 64 TWh/year | 6.1 bcm/year |

Against that market size, existing and planned LNG capacity around the region is already large. Klaipėda LNG has maximum technical regasification capacity of about 3.75 bcm per year, or roughly 39–40 TWh. Inkoo in Finland has regasification capacity of 140 GWh per day and more than 40 TWh per year. Poland’s Świnoujście LNG terminal reached 8.3 bcm per year from 1 January 2025 after expansion. The Gdańsk FSRU project is designed for about 6.1 bcm per year.

The comparison is not a simple capacity-surplus argument. Klaipėda already functions as more than a Lithuanian terminal. In 2025, gas transported by Amber Grid served consumers in Lithuania, Latvia, Estonia, Finland and Poland, while Lithuanian domestic consumption was 15.9 TWh. In practice, regional flows can move north through Latvia and Estonia towards Finland via Balticconnector, or south through the Polish-Lithuanian interconnection at Santaka, depending on market demand and booked capacity. This reflects Klaipėda’s regional role and flows beyond Lithuanian demand.

But this is exactly why the bar for a new terminal is higher. A new LNG entry point would not be serving a large untouched national market. It would have to compete for regional, reserve and transit volumes in a market already surrounded by LNG options.

This does not reduce the role of Klaipėda. Geographically, Klaipėda remains the only LNG terminal directly inside the three Baltic states. It was also the critical Baltic LNG entry point when the region needed a bargaining tool against Gazprom’s pricing and supply pressure. In its first years, Klaipėda was justified above all as an energy-security project, not as a simple commercial-payback story.

The setting is now different from the early Klaipėda period. Klaipėda keeps its unique Baltic geography, but that geography no longer means the absence of external alternatives. Inkoo provides a northern LNG entry point through Finland and Balticconnector. The Polish system provides a southern route through Lithuania.

According to a written response from GAZ-SYSTEM to Baltic Focus, transmission at Santaka on the Polish-Lithuanian border is bidirectional and market-based. At the end of 2025, Poland’s total export capacity was 12.6 bcm per year, including about 2.4 bcm per year towards Lithuania at Santaka. GAZ-SYSTEM also noted that flows to date have been irregular.

That is the point. The Polish route does not have to become a dominant baseload supply channel to matter. In a small market, irregular flows can still change the bargaining environment, provide a stress-period fallback and create another price reference against Klaipėda, Inkoo and withdrawals from Inčukalns.

The Gdańsk FSRU therefore changes the commercial case for any additional LNG terminal in the north-eastern Baltic. The issue is no longer whether the region needs access to LNG. It does. The issue is whether another standalone terminal can prove market demand, tariff logic and consumer willingness to pay for one more reserve entry point.

This is especially relevant for Estonia. Elering’s proposed gas-reserve trajectory — up to 900 MW of gas-fired reserve capacity in distributed units of 90–250 MW — raises a fuel-security question. If Estonia builds gas-fired reserve capacity, it needs reliable access to fuel in stress periods. But that does not automatically point to a separate Estonian LNG terminal.

The proposed Estonian reserve scheme answers one question: where Estonia could get fast dispatchable electrical capacity. It does not fully answer another: where the fuel comes from, under stress, in winter, at what price and through which infrastructure. Without a domestic LNG entry point, Estonia’s gas-backed electricity security depends on regional access routes — Inkoo through Balticconnector, Klaipėda and the southern route through Lithuania and Latvia — as well as Inčukalns underground storage, where gas has to be injected in advance.

The security argument does not disappear. Estonia still has to consider winter stress, Balticconnector availability, storage levels and the timing of gas withdrawals. But those risks have to be weighed against utilisation and tariff risk for a new terminal.

Paldiski, the Estonian LNG option on the north-eastern Baltic coast, would now have to be assessed against a more crowded regional infrastructure map. Gdańsk raises the threshold for Paldiski: another Baltic LNG terminal would need to show a distinct commercial role in a market already surrounded by LNG options.

The development of renewables reinforces this problem. Gas is increasingly needed as reserve for stress periods, not as baseload fuel. That raises the value of access to gas, but makes stable utilisation of a new LNG terminal less likely.

In this configuration, Paldiski no longer looks like the natural next step in Estonia’s gas logic. It may still have a security argument in extreme disruption scenarios. But its commercial case has become harder to prove.

Gdańsk does not remove the Baltic need for LNG access. It changes the benchmark for new capacity. For a small regional market, the question is no longer how to obtain access to LNG, but how many paid reserve entry points the market can support.

Sources and data used

- GAZ-SYSTEM press release received by Baltic Focus, 19 May 2026: launch of the FSRU vessel for the Gulf of Gdańsk terminal.

- GAZ-SYSTEM written response to Baltic Focus on Santaka, Polish export capacity and Amber Gas Corridor.

- Amber Grid: Lithuania gas consumption in 2025 — 15.9 TWh.

- Conexus Baltic Grid: Latvian users’ natural gas consumption in 2025 — 8.7 TWh.

- Elering: Estonia gas consumption fell from 10 TWh in 2008 to 3.4 TWh in 2023.

- KN Energies / Klaipėda LNG terminal: technical regasification capacity around 3.75 bcm/year.

- Gasgrid Finland: Inkoo LNG terminal capacity — 140 GWh/day and over 40 TWh/year.

- GAZ-SYSTEM: Świnoujście LNG terminal expansion to 8.3 bcm/year from 1 January 2025.

- GAZ-SYSTEM: Gdańsk FSRU planned regasification capacity — about 6.1 bcm/year.

- Baltic Focus earlier analysis on Estonia’s post-oil-shale energy choice and Elering’s proposed gas-reserve trajectory.