Vilniaus prekyba, the Lithuanian private holding that controls Maxima, reported €8.5bn in revenue in its 2025 annual results. But this is not only a story about one Lithuanian company. It is a useful entry point into a wider regional question: how do the largest retail groups in Latvia, Lithuania and Estonia treat the Baltics as one operating space — and why do they do it in different ways?

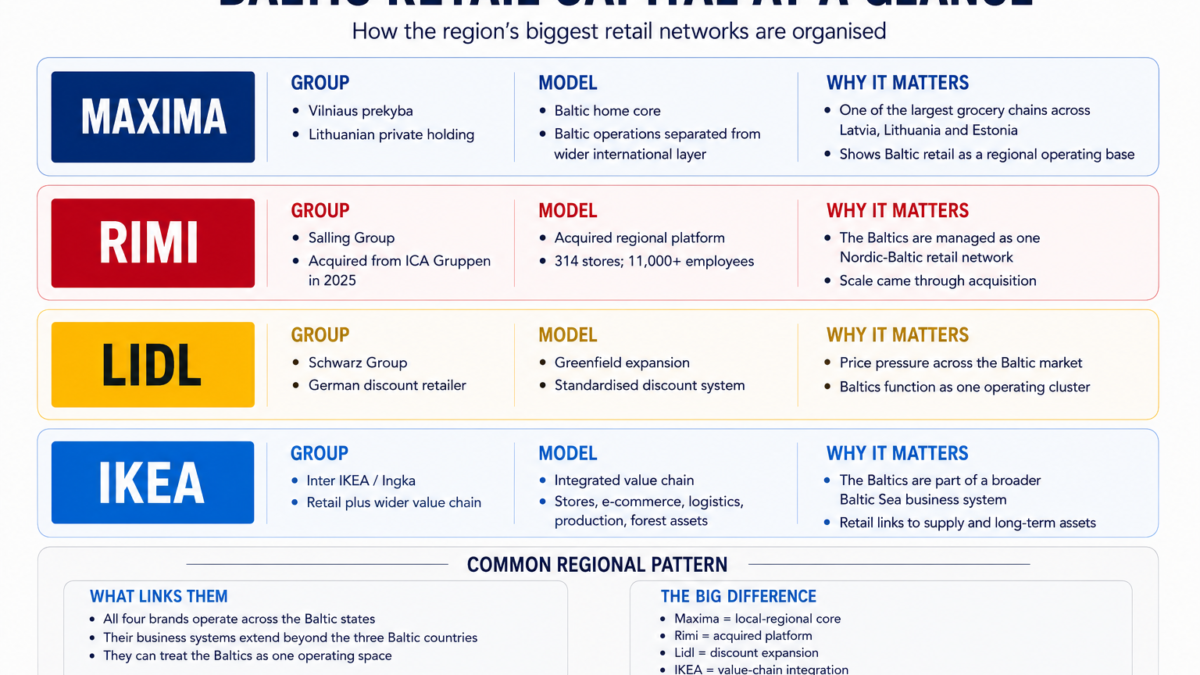

Maxima, Rimi, Lidl and IKEA are visible to Baltic consumers as retail brands. But behind those brands stand very different capital models. For Vilniaus prekyba, the Baltics are the home operating core. For Salling Group, Rimi Baltic is an acquired regional platform. For Schwarz Group, Lidl is part of a European discount system. For IKEA, the Baltics are part of a broader value chain that includes retail, digital operations, logistics, production and forest assets.

That is why Vilniaus prekyba’s annual results matter beyond Lithuania.

Vilniaus prekyba is not just the owner of a national Lithuanian retailer. Through Maxima, the group controls one of the largest grocery chains operating under the same brand across Lithuania, Latvia and Estonia. Together with Euroapotheca, Akropolis and other retail-related assets, it is one of the most important private consumer-market groups in the region.

In 2025, Vilniaus prekyba reported €8.5bn in consolidated revenue, up 4.9% year-on-year. Net profit reached €190m, up 6.1%. The group generated 59% of its revenue in the Baltic states, 23% in Poland, 14% in Sweden and 4% in Bulgaria.

These are annual-report figures, not a crisis story. But they show a clear corporate direction. Vilniaus prekyba is making the Baltics more visible as its home operating core, while businesses in Poland, Bulgaria and Sweden are being separated into a different international layer.

Maxima Grupė remains the largest part of the holding. Its revenue rose by 4.1% to more than €6.35bn in 2025. Under the wider restructuring, Maxima’s Polish and Bulgarian retail businesses — Stokrotka in Poland and T Market in Bulgaria — were transferred to Paretas B.V., a Netherlands-registered company within the Vilniaus prekyba group. The restructuring separates the Baltic retail core from businesses outside the region and is expected to be completed in the first half of 2027.

From a narrow Lithuanian angle, this is a story about the owner of Maxima. From a Baltic angle, it is a story about how large capital reads the region.

Four capital models in Baltic retail

The Baltic consumer market is now being organised by several different types of large capital at once.

Vilniaus prekyba / Maxima represents the local-regional model. The Baltics are the home core of a Lithuanian-controlled group. The restructuring does not make the Baltics smaller in the group’s story. It makes them clearer: the Baltic operations are being separated from a wider international layer that includes Poland, Bulgaria and Sweden.

Salling Group / Rimi Baltic represents the acquisition model. In 2025, Danish retailer Salling Group completed the €1.3bn acquisition of Rimi Baltic from Sweden’s ICA Gruppen. The transaction gave Salling a ready-made Baltic platform: 314 stores across Estonia, Latvia and Lithuania, more than 11,000 employees, an e-commerce platform and a centralised logistics system.

For Salling, the Baltics are not three separate small markets. They are an acquired regional retail network that can be managed as part of a wider Danish and northern European group.

Lidl / Schwarz Group represents the German discount model. Lidl is not buying a mature Baltic chain and it is not a local Baltic capital group. Its role is different: greenfield expansion, logistics discipline, standardised formats and price pressure. Recent management announcements also show a clear Baltic operating layer, with Janusz Wlodarczyk set to lead Lidl’s operations in Latvia, Lithuania and Estonia.

For Lidl, the Baltics are part of a wider European discount system. Its impact is less about corporate restructuring and more about changing the operating environment for food retail through price competition and format discipline.

IKEA represents the integrated value-chain model. Inter IKEA Group completed the acquisition of IKEA retail operations in Estonia, Latvia and Lithuania, including three full-size stores, five smaller customer meeting points, e-commerce and a digital retail development company. The acquired Baltic retail operations employed around 1,450 people and had 6.7m visitors in financial year 2024. Inter IKEA also already had purchasing, logistics and production operations in the Baltics, employing around 700 people.

The IKEA case does not stop at stores. IKEA-related structures are also expanding into Baltic forestland. In January 2026, Ingka Investments completed a €720m acquisition of forestland from Södra in Latvia and Estonia. The total area included 135,232 hectares in Latvia and 17,742 hectares in Estonia.

This makes the IKEA model broader than retail ownership. It connects stores, e-commerce, digital operations, logistics, production, wood supply and long-term forest assets.

Data card

| Indicator | Figure |

|---|---|

| Vilniaus prekyba 2025 revenue | €8.5bn |

| Vilniaus prekyba net profit | €190m |

| Share of group revenue from Baltics | 59% |

| Maxima Grupė 2025 revenue | €6.35bn+ |

| Rimi Baltic transaction value | €1.3bn |

| Ingka / Södra Baltic land deal | €720m |

Other large Baltic-wide retailers also matter. Kesko Senukai, for example, is an important DIY and home-improvement platform across Lithuania, Latvia and Estonia. But it is not the same type of case for this note. Kesko Senukai is a large regional player inside the Baltics. The focus here is different: capital groups whose wider business architecture allows them to treat the Baltics as one operating layer inside broader European or Baltic Sea systems.

The core point is therefore not the difference between food and non-food retail. That split is too narrow for the Baltic market. The more important distinction is between companies that operate in the Baltics and groups whose business systems are large enough to manage the three Baltic states as one regional space.

This is where Vilniaus prekyba’s results become more interesting. The company’s annual report confirms scale, but the restructuring clarifies the group’s operating perimeter. The Baltics are not just one part of a mixed international portfolio. They are becoming the more clearly defined home core of the Lithuanian-controlled group.

At the same time, other major players are organising the region in different ways. Salling has bought a complete Baltic grocery platform. Lidl is expanding a German hard-discount system. IKEA is integrating Baltic retail with production, logistics and forest assets.

For lenders and investors, these distinctions matter. A clearer Baltic perimeter can make cash flows, leverage and market exposure easier to assess. A Danish-owned Rimi Baltic changes the competitive map through acquisition. Lidl changes it through price discipline and format expansion. IKEA changes it through a wider value chain that reaches beyond the shop floor.

The Baltic consumer market is mature and competitive. It is not suddenly becoming a high-growth retail frontier. But it is becoming more legible as a regional operating space.

That is the real signal behind Vilniaus prekyba’s €8.5bn revenue figure.

The Baltics are no longer only three small national retail markets. For the largest players, they are a regional layer inside wider European and Baltic Sea business systems.

Signal: Baltic retail is being shaped by four capital models: Lithuanian-controlled regional ownership, Danish acquisition, German discount expansion and IKEA’s integrated value-chain logic.