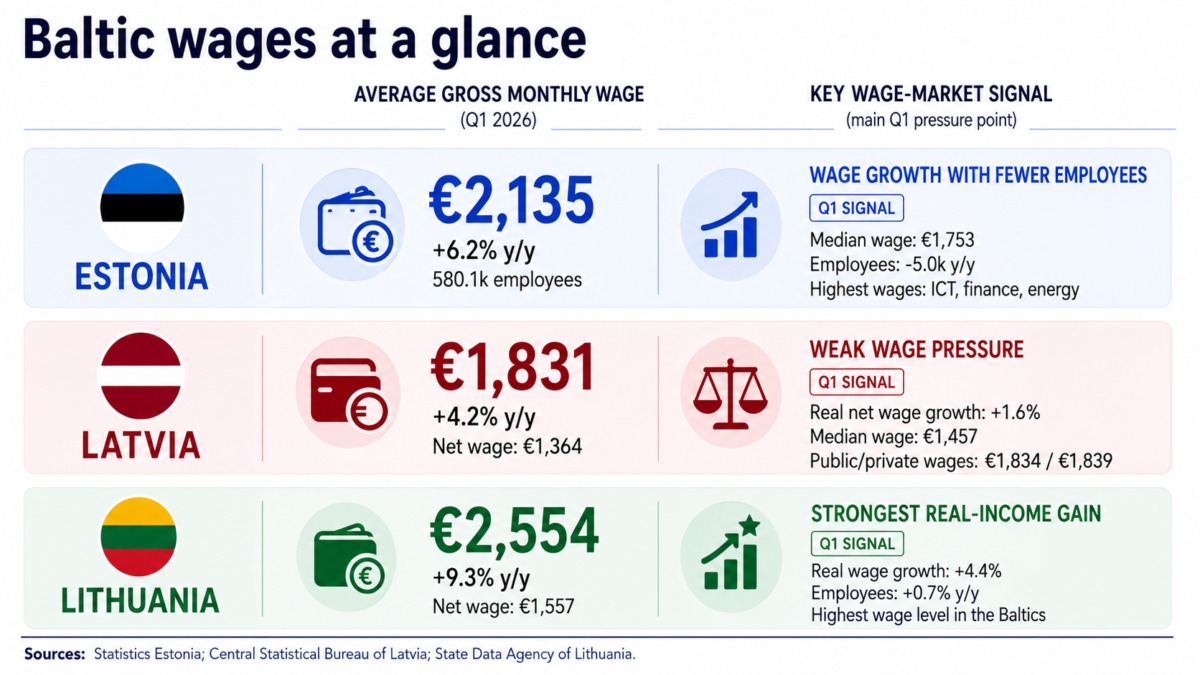

Average wages increased across all three Baltic states in the first quarter of 2026. The headline direction was similar, but the labour-market signals differed between Lithuania, Estonia and Latvia.

Lithuania remained the regional leader in both wage level and wage growth. Estonia continued to show solid wage growth, although the number of employees declined. Latvia recorded the slowest wage growth, even as employment indicators improved.

Data Card: Baltic States, Q1 2026

| Country | Average Gross Monthly Wage | Annual Change |

|---|---|---|

| Lithuania | €2,554 | +9.3% |

| Estonia | €2,135 | +6.2% |

| Latvia | €1,831 | +4.2% |

This comparison uses the common indicator available from all three national statistical offices: average gross monthly wage and its annual change.

Other indicators are not fully symmetrical across national releases. Lithuania and Latvia publish net wage and real wage indicators in their Q1 wage releases. Estonia’s release used here provides average gross wage, median wage and employee numbers, but not the same net and real wage breakdown.

Lithuania

Data Card

- Average gross monthly wage: €2,554

- Annual gross wage growth: +9.3%

- Average net monthly wage: €1,557

- Annual net wage growth: +8.4%

- Real wage growth: +4.4%

- Employees: +0.7% year-on-year

Q1 Snapshot

Lithuania recorded the strongest wage growth in the Baltic region in the first quarter of 2026.

Gross wages increased by 9.3% year-on-year, while net wages rose by 8.4%. Real wage growth was also positive, at 4.4%, meaning that wage increases clearly exceeded consumer price growth over the year.

The strongest annual wage increase was recorded in publishing, broadcasting, and content creation and distribution activities. Energy supply and several service-related activities also showed strong increases.

Lithuania therefore combined three elements: the highest average gross wage in the Baltic region, the fastest nominal wage growth, and positive real wage growth.

Estonia

Data Card

- Average gross monthly wage: €2,135

- Annual gross wage growth: +6.2%

- Median gross wage: €1,753

- Employees: 580,099

- Change in number of employees: -5,000 year-on-year

Q1 Snapshot

Estonia’s average wage continued to rise in the first quarter of 2026, though at a slower pace than in Lithuania.

The highest average wages remained concentrated in information and communication, financial and insurance activities, and electricity, gas, steam and air conditioning supply.

At the same time, Statistics Estonia reported a decline in the number of employees compared with the first quarter of 2025. This makes Estonia’s wage picture different from Latvia’s: wage growth remained stronger, but the employee base contracted.

Latvia

Data Card

- Average gross monthly wage: €1,831

- Annual gross wage growth: +4.2%

- Average net monthly wage: €1,364

- Annual net wage growth: +4.5%

- Real net wage growth: +1.6%

- Median gross wage: €1,457

Q1 Snapshot

Latvia recorded the slowest wage growth among the three Baltic states in the first quarter of 2026.

Gross wages rose by 4.2% year-on-year, while net wages increased by 4.5%. Adjusted for consumer price growth, real net earnings rose by 1.6%.

This means that Latvian wages did outpace headline inflation, but only modestly. The purchasing-power signal was weaker than in Lithuania, where real wage growth reached 4.4%.

At the same time, Latvia’s labour-market data were not weak in employment terms. Wage statistics showed an increase in full-time-equivalent employees, while labour-force data pointed to a smaller but positive rise in overall employment and a stronger increase in youth employment.

The combination is therefore specific: more people were working, but wage pressure remained limited.

Latvia: Public And Private Sector Wages Almost Converged

One of the more notable details in the Latvian data is the narrowing of the public-private wage gap.

In recent annual data, Latvia’s public sector still paid more on average than the private sector. In 2024, the average gross monthly wage was €1,742 in the public sector and €1,666 in the private sector. In 2025, the gap remained visible: €1,863 in the public sector compared with €1,800 in the private sector.

By the first quarter of 2026, this difference had almost disappeared — and slightly reversed. The average gross monthly wage stood at €1,834 in the public sector and €1,839 in the private sector.

This should not be read as a simple private-sector boom. Annual wage growth in the private sector was only 4.1%, while the public sector still grew slightly faster, at 4.6%.

The point is different: the earlier public-sector wage premium has narrowed sharply, while Latvia’s overall wage growth has slowed.

For the Latvian economy, this matters for several reasons.

First, it changes the reading of household income growth. If public-sector wage increases are no longer lifting the average as strongly as before, wage dynamics depend more on private-sector demand.

Second, it matters for the state budget. Stronger public-sector wage growth in previous years supported incomes, but it also increased fiscal pressure. A narrower gap may signal a period of adjustment after earlier wage increases in education and other publicly funded areas.

Third, it matters for labour-market interpretation. Latvia is adding workers, including younger workers, but this has not yet produced strong wage pressure. The private sector is now roughly level with the public sector in average pay, but the pace of wage growth remains moderate.

This makes Latvia’s Q1 picture more specific: employment indicators improved, the public-private wage gap narrowed, but the overall wage signal remained weaker than in Lithuania and Estonia.

What The Q1 Data Show

The first quarter of 2026 does not show a single Baltic wage story.

Lithuania had the strongest wage position: the highest average gross wage, the fastest nominal wage growth and clear real wage gains.

Estonia showed continued wage growth, but against a shrinking employee base.

Latvia showed the most mixed signal: employment improved, youth employment increased, and public-private wage levels almost converged, but wage growth remained the weakest in the region.

The key issue for the second quarter is therefore specific: whether Latvia’s expanding labour market starts to create stronger wage pressure, or whether additional labour supply continues to keep wage growth moderate.