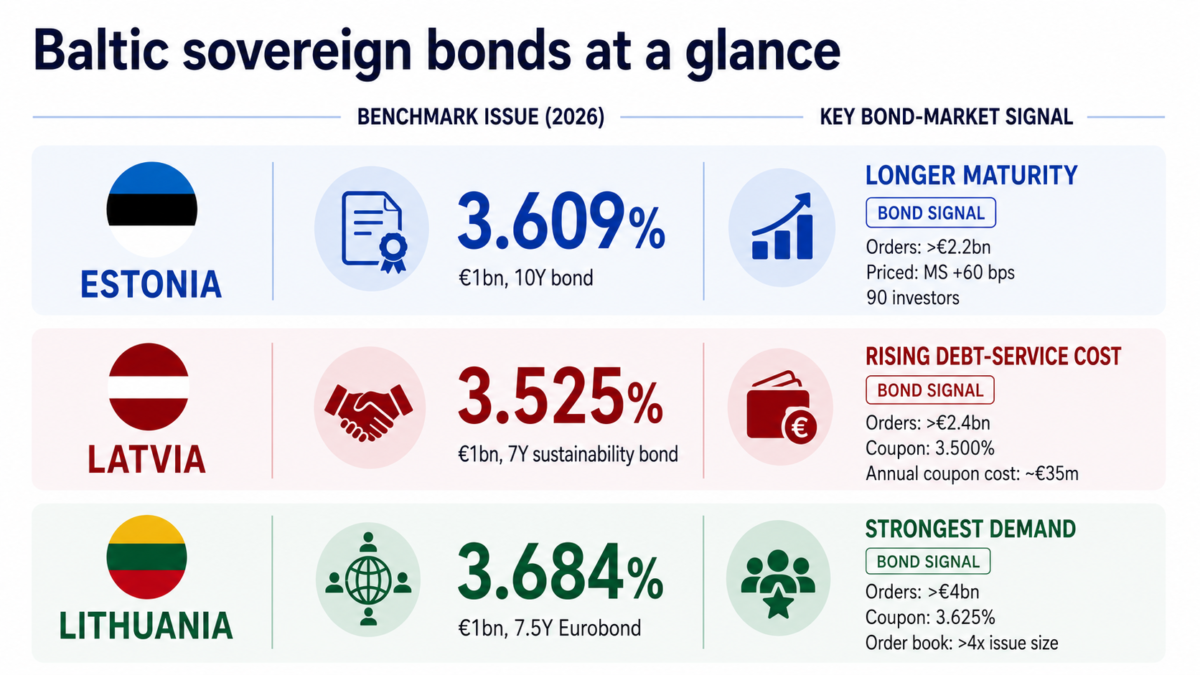

Latvia has priced a new €1bn 7-year Sustainability bond with a 3.500% coupon and a 3.525% reoffer yield.

The issue was more than twice oversubscribed: demand exceeded €2.4bn, coming from more than 70 investors, mainly European asset managers.

On paper, this is a sustainable-finance story. Latvia is issuing under its updated Sustainability Bond Framework, with proceeds allocated to green transport, biodiversity, pollution reduction, social inclusion and other sustainability-related budget expenditure.

But the regional debt-market signal is broader.

Over the past month, all three Baltic sovereigns have returned to international debt markets with benchmark-size euro issues:

| Country | Issue | Yield | Demand |

|---|---|---|---|

| Latvia | €1bn, 7Y Sustainability bond | 3.525% | >€2.4bn, 70+ investors |

| Lithuania | €1bn, 7.5Y Eurobond | 3.684% | >€4bn |

| Estonia | €1bn, 10Y bond, due 2036 | 3.609% | >€2.2bn, 100+ investors |

These are not distressed numbers. Investor demand is there. The Baltic states can still raise benchmark-size funding in euros.

But this demand has a price.

For Latvia, the new bond means roughly €35m in annual coupon payments on this single issue alone. Over seven years, that is about €245m in coupon cost, before repayment of the principal.

This figure matters because it comes on top of a broader rise in debt-servicing costs. Latvia’s Fiscal Discipline Council has warned that interest payments on public debt are increasing: from €519m in 2025 to €617m in 2026, with further growth projected to €700m in 2027 and €736m in 2028.

So the new annual coupon is not just a bond-market detail. It is one more line in a budget where interest costs are already moving higher.

For investors, Baltic sovereign bonds at around 3.5–3.7% yield and roughly 60 bps over mid-swaps, where reported, now offer visible income, an investment-grade sovereign profile and a measurable regional risk premium.

For public budgets, the same yield means a higher debt-service burden.

Estonia is an important nuance here. It is not the same credit story as Latvia or Lithuania: its fiscal profile has historically been more conservative, and its new bond has a longer 10-year maturity. But Estonia also came to the market after a weak economic cycle. Its similar headline yield should therefore not flatten the three Baltic stories, but it does make the regional pattern harder to ignore.

The sustainability label helps Latvia keep ESG-oriented European asset managers inside its investor base. But it does not remove the basic debt-market signal.

Cheap money is gone. Demand remains. And the Baltic risk premium is now visible both as investor income and as budget cost.

Source information: Treasury of Latvia, Ministry of Finance of Lithuania, Republic of Estonia / Nasdaq Baltic transaction information, Latvia Fiscal Discipline Council, Latvia Sustainability Bond Framework, Baltic Focus calculations based on issue size and coupon rates.