Latvia’s 2026 Financial Stability Report gives a calm headline: the financial system remains stable, banks are liquid and capitalised, and the sector is able to absorb shocks. But the report also materialises a more specific structural signal: Latvia’s officially recognised systemic banking core has narrowed.

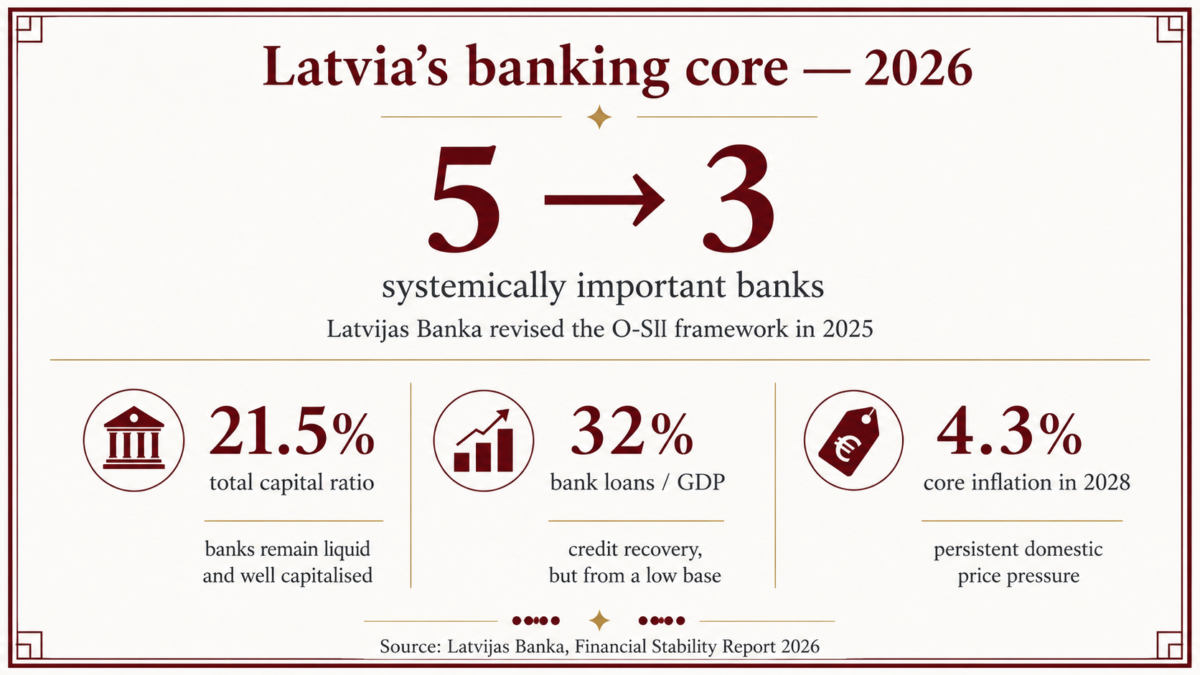

In 2025 Latvijas Banka revised the framework for identifying other systemically important institutions, or O-SII. After the revision, the number of recognised O-SII institutions fell from five to three. The remaining systemic banks are Swedbank Baltics / Swedbank, SEB banka and Citadele banka. Rietumu Banka and BluOr Bank are no longer recognised as O-SII.

Latvia’s systemic banking core

Main signal: recognised O-SII institutions narrowed in 2025.

Key numbers

- O-SII institutions: 5 → 3

- Remaining O-SII: Swedbank Baltics / Swedbank, SEB banka, Citadele banka

- No longer O-SII: Rietumu Banka, BluOr Bank

- Effect of removing O-SII requirements from Rietumu and BluOr: 0.06% of banking-sector TREA

- CCyB base rate: 1%

The change follows a revised analytical framework, not a sudden banking shock. But the outcome still matters: Latvia’s recognised systemic banking core is now centred around three institutions.

Latvijas Banka frames the change as a more proportionate framework for Latvia’s financial-sector structure. The report says the revised approach is better suited to the specifics of Latvia’s financial sector and does not reduce the overall resilience of the banking sector. At the same time, the result is clear for readers: the official list of systemic banking institutions is shorter.

The banks themselves look strong. At the end of 2025, the sector’s total capital ratio stood at 21.5%, CET1 at 19.2%, the leverage ratio at 9.0%, LCR at 206.7% and NSFR at 154.3%. The share of non-performing loans was 2.7%. These figures support the central stability message: the weak point in the report is not immediate bank solvency or liquidity.

The more important question is what sits around the banks. Credit has revived, but from a low base. In March 2026, domestic loans to non-financial companies and households were up 11.8% year on year. Loans to companies grew by 13.3%, while household loans increased by 10.3%, including 9.7% growth in housing loans.

Yet bank loans to companies and households still stood at only 32% of GDP at the end of 2025. Latvijas Banka also notes that part of the credit acceleration reflects lower interest rates, delayed demand and incentives linked to the solidarity contribution mechanism. The recovery is visible, but it is not yet proof of a deep and self-sustaining credit cycle.

Credit recovery from a low base

Main signal: credit is growing again, but Latvia remains a shallow-credit economy.

Key numbers

- Domestic loans to companies and households: +11.8% YoY

- Loans to non-financial companies: +13.3% YoY

- Household loans: +10.3% YoY

- Housing loans: +9.7% YoY

- Bank loans to companies and households / GDP: 32%

Credit growth has returned, but the banking-credit base remains low. That limits how much lending can support investment, housing supply and productivity growth.

Borrowers remain broadly resilient. Latvijas Banka describes household payment discipline as very good. The deterioration in corporate credit quality has so far affected a narrow group of borrowers. But the report also points to pressure ahead: higher energy costs, labour costs and expected EURIBOR dynamics may weigh on company profitability and debt-servicing capacity.

This matters because Latvia’s labour market is already tight. Unemployment is forecast to fall from 6.7% in 2026 to 6.3% in 2028. Nominal gross wage growth remains high, though it is not accelerating: 7.4% in 2026, 7.3% in 2027 and 7.5% in 2028. That supports household income, but it also keeps pressure on company costs if productivity does not improve.

Inflation adds another layer. Headline inflation is forecast at 3.6% in 2026, 3.8% in 2027 and 3.4% in 2028. Core inflation, however, is expected to rise from 3.3% in 2026 to 4.0% in 2027 and 4.3% in 2028. This configuration matters because easing headline inflation does not necessarily mean that domestic price pressure is disappearing.

Wages, inflation and household pressure

Main signal: wages still rise faster than headline inflation, but core inflation is expected to become stickier.

Key numbers

- Nominal gross wage growth: 7.4% in 2026; 7.3% in 2027; 7.5% in 2028

- Headline inflation: 3.6% in 2026; 3.8% in 2027; 3.4% in 2028

- Core inflation: 3.3% in 2026; 4.0% in 2027; 4.3% in 2028

- Unemployment forecast: 6.7% in 2026; 6.5% in 2027; 6.3% in 2028

This is not a real-wage collapse. But if food, fuel, utilities and basic services absorb more household income, wage growth may translate into weaker discretionary demand than the headline wage figures suggest.

The fiscal layer is also becoming more visible. Defence spending and public investment support growth, but Latvijas Banka warns that delayed improvement in the return on public spending increases the risk of sharper fiscal and tax-policy changes in the future. In the report, this is identified as a systemic vulnerability, especially in a slower-growth environment.

The overall conclusion is not that Latvia has a visible banking-stability problem. The report says the opposite: banks are liquid, capitalised and resilient.

The sharper 2026 signal is structural. Latvia’s recognised systemic banking core has narrowed from five institutions to three. Credit is growing, but from a low base. Labour is scarce. Core inflation is forecast to rise. Fiscal pressure is building. The risk is not a visible bank failure scenario. It is a more concentrated financial structure operating inside an economy with limited labour, shallow credit depth and rising policy pressure.