Not only online shoppers. The new charge reaches rail corridors, Polish warehouses, Baltic parcel operators and the logistics system built around low-value imports.

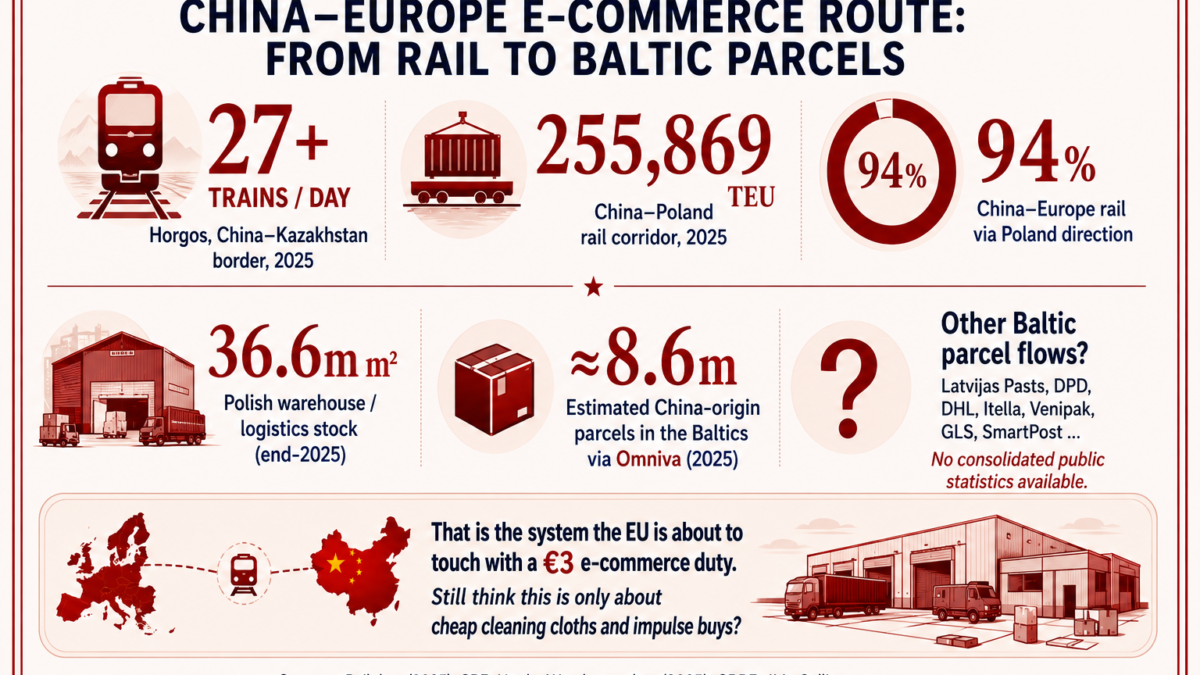

At Horgos, on China’s border with Kazakhstan, an average of more than 27 China–Europe freight trains were processed every day in 2025. On the European side, the China–Poland rail corridor handled 255,869 TEU. Through Omniva alone, an estimated 8.6 million China-origin parcels reached the Baltic market in 2025.

The EU’s new €3 e-commerce duty is not about a few hundred cheap household items moving quietly through the post.

It targets low-value imports, but those imports already move through an industrial logistics system: Central Asian rail corridors, Polish terminals, warehouses, customs data, postal operators, parcel lockers and road transport.

From 1 July 2026, the EU will add a temporary €3 customs duty to low-value goods entering the bloc from outside the EU. Politically, the measure is linked to Chinese e-commerce platforms. Economically, it reaches much further.

The duty is not a simple “€3 per parcel” charge. It is applied by customs classification inside a consignment. Five T-shirts may count as one item category. A T-shirt and a watch may count as two. That turns product data, customs codes, bundling and platform checkout logic into part of the logistics cost.

Data card 1 — EU low-value e-commerce scale

| Indicator | Figure |

|---|---|

| Low-value e-commerce consignments entering the EU, 2024 | 4.6bn |

| Low-value e-commerce parcels/items entering the EU, 2025 | 5.8bn |

| Share from China, 2024 | over 90% |

| Temporary duty | €3 |

| Low-value threshold | €150 |

| Applies from | 1 July 2026 |

The “low-value” label is customs language. It is not a consumer reality. A €100 or €150 order can still matter to a household budget, especially after several years of inflation and pressure on purchasing power.

The consumer sees a cheap order. The economy behind it sees route density, sorting capacity, warehouse demand, rail access charges, customs processing, last-mile networks and platform responsibility.

Poland is the hub layer

Poland is the clearest regional example of how Chinese-linked e-commerce becomes European logistics infrastructure.

In 2025, the China–Poland rail route accounted for about 94% of China-to-Europe rail freight flows, with 255,869 TEU moving on that corridor. Rail remains smaller than ocean shipping, but it is already large enough to support terminals, customs activity, warehouse demand and redistribution flows.

Poland is also one of Europe’s major warehouse markets. By the end of 2025, its modern warehouse and logistics stock exceeded 36.6 million square metres. This is the physical layer that turns imported goods into European inventory.

Chinese-linked e-commerce is already embedded in that structure. SHEIN’s logistics hub near Wrocław is expected to offer up to 740,000 square metres of logistics space at full capacity and support around 5,000 jobs in Lower Silesia. This is not the economics of isolated parcels. It is warehouse space, labour, sorting systems, packaging, transport contracts and fulfilment capacity.

Data card 2 — Poland: Europe’s hub layer

| Indicator | Figure |

| China–Poland rail freight corridor, 2025 | 255,869 TEU |

| Share of China–Europe rail flows via Poland direction | 94% |

| Modern warehouse/logistics stock in Poland, end-2025 | 36.6m m² |

| SHEIN Wrocław logistics hub, full capacity | up to 740,000 m² |

| SHEIN jobs footprint in Lower Silesia / Poland | ~5,000 |

The flow also pays into infrastructure. Rail operators pay for access to railway networks. Trucks moving goods from terminals and warehouses use road infrastructure and toll systems. Poland is therefore not only exposed to Chinese imports. It captures value from their movement.

That is the key point. Chinese goods are not only a burden on European retail. They also feed European logistics.

The Baltics are the receiving layer

The Baltic states are not a hub on Poland’s scale. Their role is different: they are small end-markets connected to larger European logistics infrastructure.

But the Baltic layer is measurable.

PHH Group, the owner of Pigu.lt, 220.lv and Kaup24.ee, reported 8.5 million customer orders over five years for Pigu.lt Marketplace and more than €265 million in sales. In 2025, Pigu said that after reducing Chinese sellers’ products, its assortment fell from 15 million to 8.3 million products.

That figure should not be read as an effect of the new €3 duty, which starts only in 2026. It shows something else: Baltic marketplaces already have a Chinese-seller and long-tail assortment layer, and that layer can be adjusted when platform risk, compliance or seller quality becomes an issue.

Omniva shows the last-mile layer. In 2025, the group delivered 36 million parcels across the Baltic states and more than 50 million worldwide. According to Omniva, 24% of parcels arriving in the Baltics originated from China.

If that share is applied to the full annual Baltic parcel volume — an estimate, not a separate figure published by Omniva — it would imply roughly 8.6 million China-origin parcels handled through Omniva’s Baltic network alone.

Data card 3 — Baltic last mile: Omniva, 2025

| Indicator | Figure |

| Parcels delivered across the Baltic states | 36.0m |

| Share of Baltic parcels originating from China | 24% |

| Estimated China-origin parcels in the Baltics | ≈8.6m |

| Omniva parcels worldwide | over 50m |

| Omniva revenue | €154.7m |

Estimate: 36.0m Baltic parcels × 24% China-origin share ≈ 8.6m China-origin parcels.

These are proxy indicators, not a full dataset for Chinese e-commerce. But they are enough to show the structure. The Baltics are not outside the system. They are connected through marketplaces, postal operators, parcel lockers and delivery networks.

For postal and parcel operators, the €3 duty is therefore not only a consumer-price issue. It may change parcel volumes, order consolidation, sorting workload and the economics of international transit.

Air cargo is not the cheap-goods channel

Tallinn also shows why the logistics picture should not be flattened.

Freight and mail through Tallinn Airport reached about 12,400 tonnes in 2025, up 33% from 2024. Chinese cargo has appeared in Tallinn-related air-freight reporting, but this should not be confused with the main route for ultra-cheap goods.

Air freight is too expensive for most €2–€3 items. Its relevance is different: higher-value, urgent, lightweight or platform-priority flows. The cheap mass does not normally fly as one isolated T-shirt. It is consolidated, routed, stored, sorted and redistributed.

The point is not that every Baltic parcel enters through Tallinn. The point is that the Baltic logistics layer is not only a mailbox. It includes air cargo, marketplaces, postal systems, lockers, road delivery and links to European warehouse stock.

The offer may narrow, not disappear

The likely result is not that low-value goods disappear. The more likely result is that their route and pricing structure change.

One observable market development is that the European-facing offer is already shifting. Ultra-low-price goods have not disappeared, but they appear less dominant than during the first expansion of cross-border marketplaces. A larger share of the visible assortment now starts at higher price points and is increasingly fulfilled from inventory already located inside the EU.

For Baltic consumers, this may mean fewer direct €2–€3 impulse items from China and more goods starting around €9–€10 from EU-based warehouses. Delivery may become faster and administratively cleaner, but the entry price may be higher.

That is not a disappearance of Chinese goods. It is a change in the route.

The merchant function returns

The old import-retail chain selected goods, carried customs and logistics costs, held stock and sold the product through a local shelf.

Cross-border platforms unbundled that chain. They gave consumers direct access to a much wider catalogue, including low-value goods that local retailers often cannot stock economically.

The EU is now trying to put part of that merchant function back into the digital trade route.

Someone must classify the goods, carry responsibility, pay duties, handle compliance and make the cost of entry into the European market visible. That function may now sit with a platform, an importer, a fulfilment operator, a warehouse inside the EU, a postal operator or a marketplace seller.

This may help some European retailers. If the price gap narrows, a buyer may prefer a local or EU-based seller with faster delivery, simpler returns and clearer consumer rights.

But the effect should not be overstated. Platforms compete not only on price. They also offer product variation that traditional retailers often cannot stock economically. A local shop may carry one or two versions of a small household item. A marketplace can show many sizes, colours, formats and accessory variants.

The duty may narrow the price gap. It does not remove the assortment gap.

Europe is not only a victim of the flow

The EU debate often presents low-value imports as pressure on European retailers and producers. That pressure is real.

But the economic picture is not one-sided.

The same flow that pressures local retail also fills warehouses, generates rail traffic, supports parcel operators, keeps sorting centres busy and feeds road distribution. Poland’s rail corridor, warehouse stock and SHEIN logistics hub are not side details. Omniva’s 36 million Baltic parcels are not side details either.

European operators already earn from the movement, storage, sorting and delivery of these goods.

That does not make the retail concern irrelevant. European shops carry inventory, pay local costs, handle compliance and provide consumer rights. But the conflict is not simply “European production versus Chinese parcels”. It is also about who controls the import route, who carries compliance costs, who captures the margin and where the merchant function sits.

The EU treats low-value e-commerce as a customs, fairness and compliance problem. The market has already turned it into a logistics ecosystem.

The €3 duty will therefore affect more than online shoppers. It will test the platforms, but also the European infrastructure that has grown around their flows: Central Asian rail corridors, Polish terminals and warehouses, Baltic last-mile networks, postal operators, marketplaces, customs systems and road transport.

The EU is also preparing a separate handling fee for low-value parcels, with the final amount and timing still to be confirmed. Together, these measures point in one direction: the era of almost invisible direct small imports is ending.

The political focus may be China-linked platforms. But the economic effect is wider. The EU is not only taxing a parcel. It is changing the route by which low-value goods enter, move through and become part of the European economy.