Asked about airBaltic’s future in a 16 June interview on Latvian Television, Prime Minister Andris Kulbergs said that the state had to “stop acting as an ATM”.

The demand is understandable. airBaltic needs a credible business plan, a financing solution and a clear answer for creditors before its next major payment deadline.

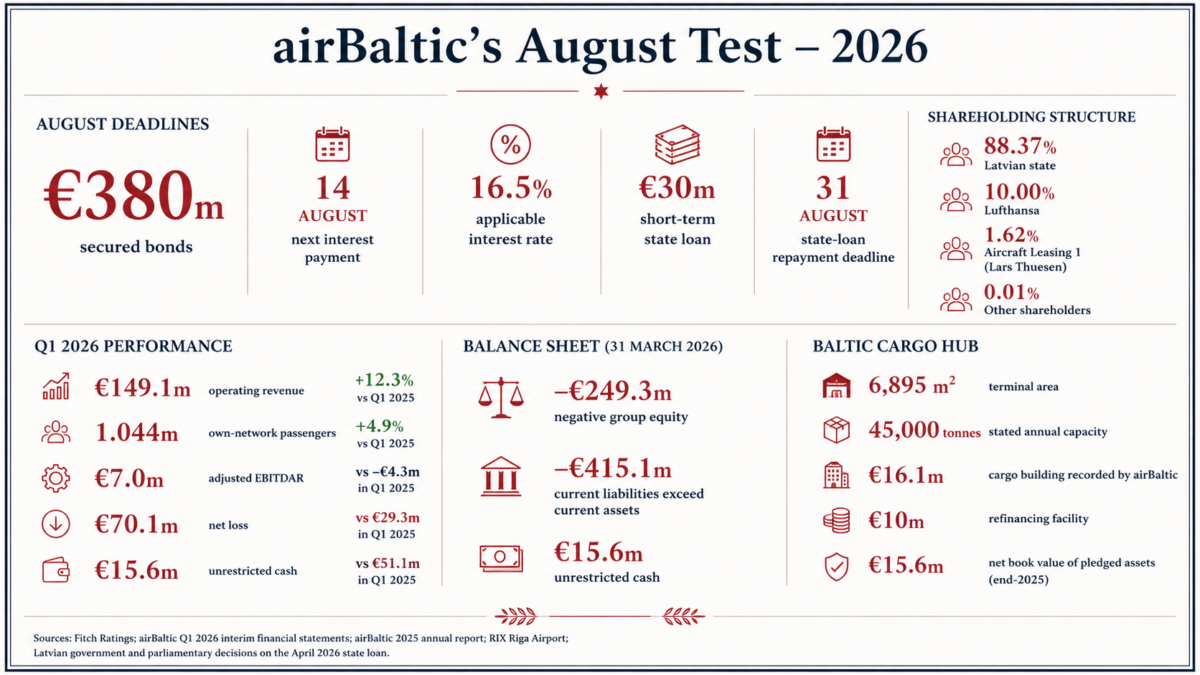

But Latvia is not an external rescuer dealing with an ordinary private debtor. At the end of the first quarter of 2026, the Latvian state held 88.37% of airBaltic’s shares, Lufthansa held 10%, Aircraft Leasing 1 held 1.62%, and the remaining 0.01% was held by other shareholders.

Latvia is therefore not merely being asked to support the company from outside. It is the dominant shareholder of a business whose financial structure developed under continuous state control, while the state appointed supervisory bodies, influenced strategic decisions and retained control over the company.

The central question is therefore not only whether the current management can solve the crisis.

It is whether Latvia can demand that airBaltic resolve the crisis as an ordinary commercial company while refusing to account for the state’s own role in creating the structure now being rescued.

On 26 June, airBaltic announced through Euronext that it would not fund its Bonds Service Reserve Account to the required level while completing a revised business plan and assessing financing alternatives.

On 7 July, Fitch placed the airline’s CCC− rating on Rating Watch Negative, citing increased liquidity pressure and a higher probability of a distressed debt exchange or another form of restructuring. Fitch said the reserve-account decision increased the rate applicable to the next quarterly payment from 14.5% to 16.5%.

That payment is due on 14 August.

The €30 million short-term state loan provided in April must be repaid by 31 August. According to airBaltic’s accounts, the loan does not constitute a permanent addition to the company’s capital base.

The airline and its controlling shareholder therefore have only weeks to agree on a financing route.

AIRBALTIC’S AUGUST DEADLINES

€380 million secured bonds

14 August next quarterly interest payment

16.5% applicable interest rate

€30 million short-term state loan

31 August state-loan repayment deadline

BALTIC BIG PICTURE

The bond payment and state-loan deadline leave little time to agree on a financing structure.

Sources: Fitch Ratings; airBaltic Q1 2026 interim financial statements; Latvian government and parliamentary decisions on the April 2026 state loan.

A commercial debtor under state control

Legally, airBaltic remains responsible for its own liabilities. Its bonds are not Latvian sovereign debt, and the state has not formally guaranteed repayment to creditors.

At the same time, the company is registered as a legal entity significant to national security. Under Latvia’s National Security Law, transactions affecting significant participation, decisive influence, control or strategically important assets may require government approval.

The national-security status does not improve the legal position of bondholders.

It does, however, mean that any recapitalisation or restructuring involving a material change of ownership or control would remain linked to decisions by the Latvian government.

Creditors are therefore dealing with a commercial debtor whose liabilities remain formally separate from those of the state. Potential investors, however, must assess a company whose dominant shareholder, strategic status and possible changes of control remain inseparable from government decisions.

This is the first asymmetry in Latvia’s position.

The state insists that airBaltic is commercially responsible for its debts while retaining decisive influence over the corporate structure within which those debts must be resolved.

A working airline with a balance-sheet crisis

airBaltic’s first-quarter results do not support the argument that weaker passenger demand was the main cause of the deterioration.

Operating revenue increased by 12.3% to €149.1 million.

The number of passengers carried on airBaltic’s own network rose by 4.9% to 1.044 million.

Adjusted EBITDAR improved from a negative €4.3 million in the first quarter of 2025 to a positive €7 million in the first quarter of 2026.

The net loss nevertheless widened from €29.3 million to €70.1 million.

AIRBALTIC Q1 2026

€149.1 million operating revenue — +12.3%

1.044 million own-network passengers — +4.9%

€7.0 million adjusted EBITDAR

€70.1 million net loss

€15.6 million unrestricted cash

BALTIC BIG PICTURE

Higher revenue and improved fleet availability did not offset currency losses, financing costs and rising non-fuel expenses.

Source: airBaltic Q1 2026 interim financial statements.

The difference is visible in the financial statements.

A €23 million foreign-exchange gain recorded in the first quarter of 2025 became a €14.4 million foreign-exchange loss in the first quarter of 2026.

Finance costs remained at €26.8 million.

Depreciation and amortisation increased to €33.1 million.

Normalised unit costs excluding fuel and emissions rose by 6.3%, driven mainly by personnel, passenger-service, navigation and terminal costs.

The Pratt & Whitney engine disruption was no longer the immediate explanation for the financial result. airBaltic reported that no aircraft were unavailable specifically because of engine-related problems during the first quarter of 2026, compared with an average of 13 aircraft a year earlier.

Fleet availability improved. Passenger numbers increased. Revenue grew.

The company’s existing financing and cost structure nevertheless absorbed the operational gains.

At 31 March, airBaltic had negative group equity of €249.3 million.

Current liabilities exceeded current assets by €415.1 million.

Unrestricted cash stood at only €15.6 million.

This is not an airline that has stopped working. It is an airline whose balance sheet leaves little room for delay, volatility or another unsuccessful financing round.

New management, inherited commitments

The government has increasingly placed public responsibility for resolving the crisis on airBaltic’s current leadership.

On 6 July, Kulbergs said that the company could no longer approach the state for money without an “ironclad” plan. He also said that the state had demonstrated that it was not a good airline manager.

The second statement warrants more attention than it has received.

If the state was not a good manager of its airline, why should the full financial consequences of that management now be assigned solely to the airline’s latest executives?

The governance structure currently expected to produce a solution was largely formed during 2025.

On 11 February, shareholders appointed an interim supervisory board chaired by Andrejs Martinovs.

The board dismissed long-serving chief executive Martin Gauss on 7 April after the Ministry of Transport initiated a vote of no confidence.

Pauls Cālītis then led the company on an interim basis.

The supervisory board was expanded in August, including the appointment of a Lufthansa Group representative following the strategic investor’s entry into the company.

Erno Hildén took office as chief executive on 1 December 2025.

The current supervisory and executive structure was therefore appointed after the €380 million bond issue, the previous fleet-growth strategy and most of the company’s existing long-term commitments had already been established.

Since then, airBaltic has agreed to return two Airbus A220-300 aircraft early, reducing its fleet to 54 aircraft.

No additional aircraft deliveries are planned in 2026.

The company has also declined to reconfirm its previous target of operating a fleet of close to 100 aircraft by 2032.

During the summer season, up to 25 aircraft are expected to operate for Lufthansa Group airlines and Air Serbia. During winter, the projected number falls to six.

These decisions do not yet define the final business model.

They do show that the new leadership is already reassessing fleet size, future deliveries and the balance between airBaltic’s own network and ACMI operations.

Management is responsible for making sound decisions now.

But it did not create the starting position from which those decisions must be made.

Shareholder responsibility does not disappear when the cabinet changes

This is where Latvia’s model of political accountability becomes problematic.

Successive governments have treated shareholder responsibility as if it were limited to the term of a particular cabinet.

Each cabinet inherits the state’s controlling stake, but the financial consequences of earlier state-approved decisions are increasingly presented as a management problem belonging to the company.

The shareholder remains the same.

Only the government acting on its behalf changes.

Its responsibility should therefore remain continuous as well.

Instead, an asymmetry of accountability emerges. Management remains answerable for the company’s accumulated financial position, including commitments made before its appointment, while the state’s responsibility as controlling shareholder is effectively reset after every political transition.

This concern is not new.

In May 2025, Latvia’s State Audit Office concluded that the state had acted less like a demanding and competent owner of airBaltic than as a source of funds from which the company could draw. It also found that an effective mechanism for monitoring the use of state investment in the airline had still not been established.

The audit focused primarily on public support provided during 2020–2022 and on the conduct of officials responsible for overseeing it. Its scope was narrower than the present financing crisis.

But its conclusion reinforces the broader point: the weakness was not confined to company management. It also concerned how the state exercised its ownership role.

The state retains the right to appoint supervisory bodies, influence strategic choices, protect its control and approve changes of ownership.

When the financial consequences arrive, however, airBaltic is once again described as an independent commercial company whose latest management must solve the problem.

Airport infrastructure on airBaltic’s balance sheet

The Baltic Cargo Hub provides a concrete example of why the crisis cannot be reduced to management performance alone.

The Latvian government has demanded improvements in airBaltic’s financial position for years.

During the same period, the state remained the controlling shareholder while the airline’s capital was committed to infrastructure whose benefits extended beyond its immediate flight operations.

RIX communications present the Baltic Cargo Hub as part of Riga Airport’s broader cargo and logistics development.

The completed building, however, is recorded on the balance sheet of the airBaltic parent company rather than that of the airport.

Riga Airport launched a tender in November 2020 for land and the construction of a multimodal logistics centre.

airBaltic won the tender, and the parties signed a land-reservation agreement in April 2021.

The original project envisaged a facility of approximately 6,000 square metres, annual capacity above 30,000 tonnes and bank financing.

By the start of construction in February 2024, the planned area had increased to 6,895 square metres and the stated annual capacity to 45,000 tonnes.

RIX and government communications described the project as strengthening Riga Airport, Latvia’s aviation logistics and the country’s competitiveness.

Under the project structure, RIX provided the land and granted the building rights.

Air Baltic Corporation financed the construction, recognised the completed terminal on its balance sheet and assumed the associated investment and utilisation exposure.

Both companies were controlled by the Latvian state through the Ministry of Transport.

The state was therefore represented on both sides of the decision over how the land, investment and project risk would be allocated.

BALTIC CARGO HUB

6,895 m² terminal area

45,000 tonnes stated annual capacity

€16.1 million cargo building recorded by airBaltic

€10 million refinancing facility

€15.6 million net book value of pledged assets at end-2025

BALTIC BIG PICTURE

RIX incorporated the terminal into its cargo-development system, while the investment and financing exposure remained with airBaltic.

Sources: RIX Riga Airport; airBaltic 2025 annual report; airBaltic Q1 2026 interim report.

The timing matters.

At the end of 2023, before construction began, airBaltic already had negative group equity of €48.3 million.

Gross debt stood at €1.15 billion.

Cash, including restricted cash, amounted to €29.1 million.

The company reported a profit for 2023, but its capital position was already weak.

After completion, the cargo building was recorded at approximately €16.1 million.

In August 2025, airBaltic obtained a €10 million facility to refinance the construction investment.

The loan was secured by the building rights and the building itself. The pledged assets had a net book value of €15.6 million at the end of 2025.

The question is not whether Riga Airport needed a modern cargo terminal.

The question is why the investment, ownership and utilisation exposure for infrastructure serving the airport’s wider cargo system was assigned to an airline whose own capital position was already weak.

That decision was made within a system in which the Latvian state controlled both parties.

The current supervisory board and executive management inherited the building, the refinancing facility and their effect on airBaltic’s balance sheet.

The original allocation of capital and risk was decided earlier.

What must be decided before 14 August

The publicly identifiable options include new external capital, an agreement with bondholders, additional state support, changes to the bridge-loan terms or formal restructuring if other financing routes cannot be completed.

The restructuring scenario is no longer theoretical. Bondholders have engaged legal advisers ahead of possible negotiations over the terms of the €380 million debt, while the notes have traded at deeply distressed levels.

This does not determine the outcome.

It does show that creditors are already preparing for a process extending beyond an ordinary refinancing discussion.

Each option would have different consequences.

New investors may demand ownership, governance or control rights.

Bondholders may require higher returns, additional security or revised repayment terms.

Further state support would again raise questions about the amount of public money required and the conditions attached to it. It would also have to be assessed within the constraints of EU state-aid rules.

A formal restructuring could alter the treatment of creditors and affect the company’s future ownership structure.

airBaltic’s first-quarter report states that external advisers are assessing its capital structure and strategic alternatives.

The previous IPO process has been suspended.

Management says it is in dialogue with stakeholders, including the Latvian state.

The government has not yet publicly identified which financing route it considers acceptable.

It has not explained what ownership or governance rights it would be prepared to offer in exchange for new capital.

Nor has it explained how a restructuring involving changes of control would interact with airBaltic’s national-security status.

The 14 August payment is therefore more than a coupon date.

It is the point by which Latvia needs a clearer position on liquidity, creditor treatment, potential new capital and the state’s future role as shareholder.

Who has seen the business plan?

The public handling of airBaltic’s revised business plan has added another layer of uncertainty.

On 15 June, after a meeting lasting almost three hours with airBaltic management, Kulbergs described the plan as concrete, precise and potentially feasible.

On 6 July, however, he said that it had still not been shown to the government.

airBaltic responded that the plan had been presented on 15 June and subsequently revised.

On 9 July, the Ministry of Transport confirmed that a formal version had been submitted to the ministry and the State Chancellery for assessment.

These statements may refer to different stages of the same document.

But the distinction was not communicated clearly.

That matters because the next bond payment is due on 14 August.

Latvia still has time to act.

It has critically little time to operate without a shared understanding of what has been reviewed, what has been revised and what has been formally submitted.

In aviation, this would be described as a loss of situational awareness.

If airBaltic’s flight crews managed an aircraft in the same way, a crash would be almost inevitable.

Latvia may have a different government within months. airBaltic, however, will retain the same bonds, assets, contracts, collateral and the accumulated consequences of decisions made under state ownership.

Governments may change, but the controlling shareholder does not.

Unless Latvia recognises the continuity of its own responsibility as shareholder, each new cabinet will be able to distance itself from earlier decisions while transferring the full accumulated burden to the airline’s latest supervisory board and management.