Eesti Pank is calling for a cross-party debt anchor while Estonia’s public debt remains the lowest in the Baltics. Latvia and Lithuania show why the warning matters beyond Estonia.

Eesti Pank is calling for a cross-party debt anchor while Estonia’s public debt remains the lowest in the Baltics. Latvia and Lithuania show why the warning matters beyond Estonia.

The Estonian warning

Estonia is not facing a public-debt crisis by European standards. That is precisely why the warning from Eesti Pank president Madis Müller matters.

In a 7 May statement, Müller argued that Estonia should reach a cross-party agreement to slow the growth of public debt. His point was not that Estonia’s debt level is already high. It is that the speed of the increase is becoming politically and economically dangerous.

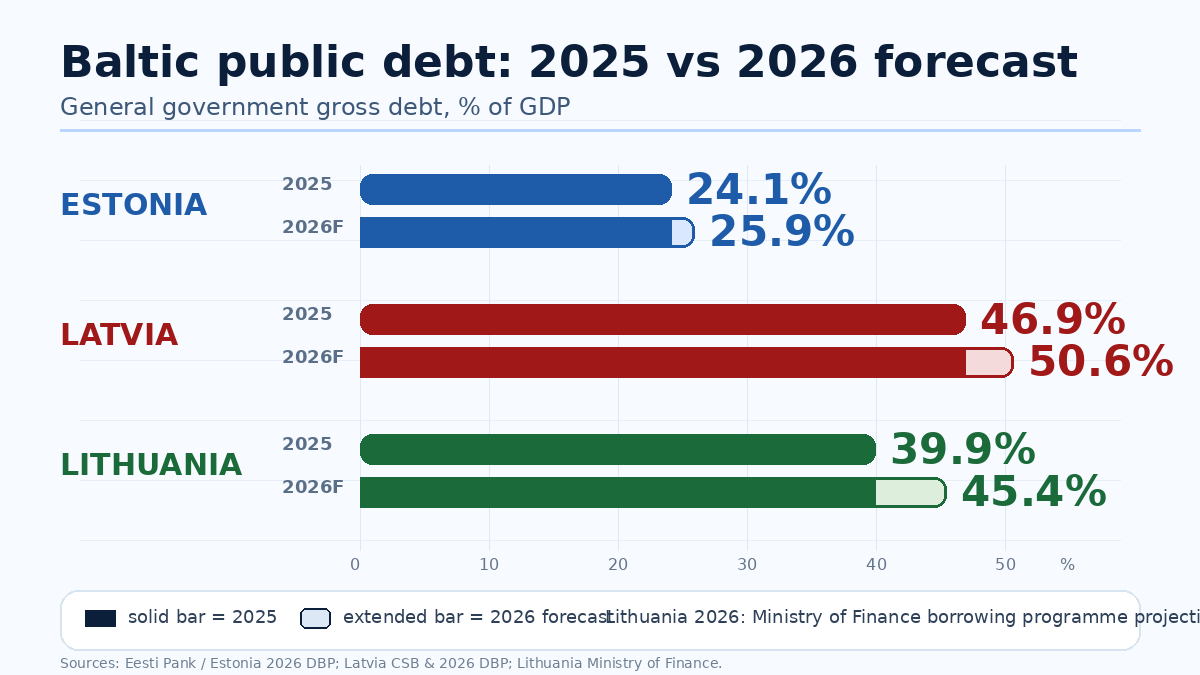

Estonia’s public debt has quadrupled in six years: from about €2.5bn in 2019 to €10bn in 2025. As a share of GDP, the level remains moderate, at about 24%. But the trajectory is much less comfortable.

This year’s planned budget deficit of 4.5% of GDP will have to be financed with additional borrowing. If spending and tax policy are not significantly adjusted, the Ministry of Finance forecast cited by Müller points to debt rising above €20bn, or 39% of GDP, by 2030.

Data card: Baltic public debt

| Country | Public debt, 2025 | Debt path / latest forecast | Main signal |

|---|---|---|---|

| Estonia | about €10bn / about 24% of GDP | Could exceed €20bn / 39% of GDP by 2030 if policy is not adjusted | Lowest Baltic debt level, but earliest political warning |

| Latvia | €20.2bn / 46.9% of GDP general government debt | Central government debt: €20.5bn at end-2025; government says defence spending will be increased while keeping general government debt below 55% of GDP | Highest Baltic debt level, still framed as moderate and manageable |

| Lithuania | around 40% of GDP | Ministry of Finance projects about €40bn / 45.4% of GDP at end-2026 | Middle case, moving quickly toward the higher-debt zone |

Latvia’s general government debt rose by €1.4bn in 2025 and reached €20.2bn, or 46.9% of GDP; the deficit was €1.1bn, or 2.5% of GDP. Lithuania’s Ministry of Finance projects that general government debt will reach about €40bn, or 45.4% of projected GDP, by the end of 2026.

Estonia: the problem is speed, not the current level

The core of the Estonian signal is simple: the problem is not the current debt ratio, but the fiscal habit that may be forming behind it.

Müller also points to the second-order effect — interest costs. In 2022, Estonia paid €28mn in debt interest. By 2030, that figure could rise to around €650mn, absorbing about 3% of all state revenues.

The central-bank argument is therefore not only about debt accounting. It is about the future room for public services, crisis response, investment and private-sector financing.

This is why the proposal is not merely another budget rule. It is an attempt to create pre-market discipline: to set a political debt anchor before markets start pricing the absence of one.

A debt anchor, not just another fiscal rule

The institutional part of the warning is equally important.

Estonia has already adopted budget rules that should limit debt growth after the end of the defence-spending exception from 2029. But Eesti Pank argues that the current framework may not be sufficient to stabilise the debt burden.

The law includes a 30% debt clause, after which annual deficits should be more strictly limited, but it does not create a clear debt anchor or target level.

Müller’s conclusion is that a broader political agreement is needed — one that would hold beyond a single coalition and a single electoral cycle.

Such an agreement would not be easy in Estonia either. A debt anchor sounds technocratic, but it quickly becomes political because parties disagree on the mix of tax increases, spending cuts and defence exceptions. The difficulty is not only to agree that debt should be stabilised. It is to agree who pays for that stabilisation, when, and through which policy mix.

That is why Müller’s proposal matters. He is asking parties to agree first on the fiscal boundary, even if they continue to disagree on the tax and spending choices inside it.

That makes Estonia the most interesting Baltic case. It has the lowest debt level in the region, but it is the first to frame debt growth as a political architecture problem.

The denominator risk: debt depends on growth

Debt ratios are not driven only by borrowing. They also depend on the denominator — GDP.

This matters for all three Baltic states. If economic growth disappoints, debt-to-GDP ratios can deteriorate faster even without a dramatic increase in nominal borrowing. A debt path that looks manageable under a recovery scenario becomes more fragile under stagnation.

That is especially relevant for Latvia. A debt ratio close to 47% of GDP is not extreme by EU standards, but it becomes more sensitive if growth remains weak, spending pressures rise and refinancing costs increase at the same time.

Lithuania has a stronger growth profile, but its debt trajectory is still moving upward because defence and nationally financed investment are pushing expenditure higher. Estonia’s warning is built around this same logic: the country is still low-debt, but the trajectory becomes much harder to stabilise if growth does not do part of the work.

The fiscal risk is therefore not only how much governments borrow. It is whether the economy grows fast enough to keep the debt ratio stable.

Debt is no longer cheap

The warning also comes after the end of the zero-rate era.

Baltic governments could previously increase borrowing at very low servicing costs. That environment has changed. Even if the European Central Bank eases policy, new debt is no longer being issued in the world of near-zero rates.

For small euro-area issuers, the borrowing cost is not only about the ECB rate. It is also about the spread investors demand over core European debt.

Even if euro-area rates decline, Latvia’s or Lithuania’s borrowing cost can still rise relative to core Europe if investors demand a wider Baltic risk premium.

This is the difference between a calm debt ratio and a vulnerable debt model. Debt can remain below Maastricht limits and still become politically restrictive if each refinancing round absorbs more budget space.

Latvia: higher debt, calmer official language

Latvia shows why this matters.

According to Latvia’s Central Statistical Bureau, Latvia ended 2025 with general government consolidated gross debt of €20.2bn, or 46.9% of GDP. The deficit reached €1.1bn, or 2.5% of GDP, while expenditure grew faster than revenue.

The debt ratio is almost twice Estonia’s level.

The Latvian State Treasury presents the situation in a calmer frame. It stresses that Latvia’s general government debt and interest expenditure levels relative to GDP remain among the lowest in the EU and the euro area, and that rating agencies still assess Latvia’s debt and debt-servicing costs as moderate compared with its rating peers.

At the end of 2025, central government debt under the national methodology amounted to €20.5bn, up by €1.4bn over the year. The Treasury links the increase to the budget deficit, which was affected by higher defence expenditure.

This is not an immediate market-access story. Latvia can borrow. Investor demand exists. Debt remains below the Maastricht threshold. The question is different: at what point does a “moderate” debt level become a new political baseline?

Latvia’s market-risk problem

Latvia’s debt structure makes the calm official language only partly reassuring.

According to the State Treasury report cited by LETA, eurobonds issued in financial markets account for 88% of Latvia’s central government debt structure. The Treasury’s published report also states that government bonds make up most of the central government debt portfolio and highlights eurobonds in international financial markets as a core instrument of borrowing.

This does not signal immediate stress. In normal conditions, the structure works well: investors buy, demand exceeds supply, and the state can borrow on acceptable terms.

But the same structure becomes more vulnerable if the European or regional risk environment deteriorates. In a broader market shock, investors may reduce exposure to smaller sovereign issuers, especially those located close to the region’s main security frontier.

Latvia would not need to face a funding crisis for the budget impact to become real. A sell-off in Latvian bonds would not immediately change the stock of debt already issued at fixed coupons. The fiscal damage would come through repricing: higher yields on new borrowing, more expensive refinancing and a higher sovereign benchmark for the domestic economy.

The danger is not default. The danger is repricing.

Latvia’s risk is not the absence of buyers today. It is the assumption that buyers will remain available at comfortable prices tomorrow. The Latvian question is therefore not only how large the debt is, but how much of it must be continuously validated by external markets.

Credit ratings are part of the repricing channel

Credit ratings are another part of this mechanism.

Latvia still retains stable investment-grade ratings. Fitch affirmed Latvia at A- / Stable in April 2026 and forecast public debt rising from 46.9% of GDP in 2025 to 51.6% in 2027, before broadly stabilising. Moody’s affirmed Latvia at A3 / Stable in January 2026 and forecast debt rising to 49.6% of GDP in 2026, mainly because of higher defence spending.

This means that a move toward the 50% of GDP zone does not automatically trigger a negative rating outlook. The major agencies still describe Latvia’s debt position as manageable.

But the margin of comfort narrows. If higher debt is combined with persistent deficits, weaker growth, rising interest costs or a wider regional risk premium, the rating story can shift from “moderate and manageable” to “less fiscal flexibility”. That shift can widen spreads before any formal funding crisis appears.

This is why the rating channel matters for the broader argument. Repricing does not require a downgrade. Sometimes it begins with a changed perception of fiscal space.

Refinancing risk: the calendar matters

The key variable is not only the debt ratio. It is also the refinancing calendar.

If large maturities coincide with a period of higher yields, weaker investor appetite or a wider Baltic risk spread, the budget impact can appear quickly even without a formal funding crisis.

Higher yields would matter not because Latvia is close to losing market access, but because higher interest costs reduce fiscal flexibility and weaken the debt-stabilisation story.

That is where the Estonian warning becomes relevant for Latvia. Müller is not saying that markets are already closed. He is saying that a country should create fiscal discipline before markets start demanding compensation for its absence.

Latvia’s election year makes a fiscal pact unlikely now

For Latvia, this question is especially difficult to turn into an immediate political call.

Parliamentary elections are due in October 2026. Until the next Saeima and coalition are known, any cross-party fiscal pact would be more rhetorical than operational.

The Latvian relevance of Müller’s argument is therefore not “the current parliament should copy Estonia tomorrow”. It is that the next Latvian parliament may inherit a debt level already close to 50% of GDP, with defence spending, ageing, refinancing costs and weak growth all competing for space in the same budget.

Lithuania: the middle case moving upward

Lithuania completes the regional picture.

It sits between Estonia and Latvia, but its debt path is also moving upward. According to Lithuania’s Ministry of Finance, the government plans to borrow approximately €10.9bn in 2026.

The largest part of the financing will come from international markets through €4.5bn of Eurobond issuance. Another €2.8bn is planned through government securities auctions and retail savings notes, while about €3.6bn is expected from international financial institutions and the European Commission.

The borrowing need is not only about refinancing. Around €6.4bn is planned for financing the general budget deficit, while €3.8bn is designated for debt repayment. About €0.3bn is planned for state on-lent loans to other legal entities.

By the end of 2026, Lithuania projects general government debt at about €40bn, or 45.4% of projected GDP.

This makes Lithuania the hinge case in the Baltic debt map. It is not yet Latvia, but it is no longer close to Estonia either. Its 2026 borrowing programme shows how quickly the middle Baltic case is moving into the higher-debt zone.

The defence exception can become a structural deficit

Defence spending is often treated as an exceptional reason for higher borrowing. In the Baltic region, this is politically understandable. The security environment has changed, and defence is not a discretionary luxury.

But the fiscal risk depends on whether these are temporary procurement peaks or a new permanent expenditure floor.

Equipment purchases can be one-off. Personnel, maintenance, ammunition stocks, infrastructure and readiness costs are recurring.

Defence spending is different from ordinary discretionary expenditure. Once security commitments, personnel, infrastructure and procurement chains are expanded, they become politically and operationally difficult to reverse.

This is the risk of a defence trap: an emergency fiscal exception can become a permanent structural deficit.

Demography makes moderate debt less comfortable

A 45–50% debt ratio does not mean the same thing in a young, fast-growing economy and in an ageing economy with a shrinking labour force.

In the Baltics, the debt ratio is only one measure of fiscal pressure. Another is the future burden per worker. As populations age, pension, healthcare and long-term care costs rise, while the working-age tax base becomes harder to expand.

This is why delaying adjustment is costly. The same debt stock may have to be serviced by a less favourable demographic structure.

For Latvia and Lithuania, this makes a move toward the 50% of GDP zone more important than the comparison with the EU average suggests.

The adverse scenario is not a debt crisis

The adverse scenario for the Baltics is not an immediate debt crisis.

It is a combination of weak GDP growth, persistent defence-related deficits, higher refinancing costs, demographic pressure and wider Baltic risk spreads.

In that scenario, public debt can remain below Maastricht limits while still crowding out future spending choices.

That is the key point. Debt does not need to become unsustainable overnight to become politically limiting. It only needs to become expensive enough to narrow the room for future governments.

The Baltic debt question

This gives the Baltic debt debate a clear structure.

Estonia is sounding the alarm early, at around 24% of GDP, because it sees a fast-moving trajectory. Lithuania is moving toward 45.4% of GDP in 2026, with a borrowing programme of about €10.9bn. Latvia is already at 46.9%, while still presenting the level as moderate and manageable.

The issue is not whether Baltic debt levels are high compared with southern Europe or the EU average. They are not. The issue is whether the region has political mechanisms to prevent defence-era borrowing from becoming a permanent fiscal habit.

That is why Müller’s proposal is more than an Estonian domestic intervention. It is an early Baltic warning.

Public debt can remain technically manageable long after it has become politically normal. Estonia is trying to define a brake before that happens. Latvia and Lithuania show what the next stage of the discussion may look like when the debt base is already much higher.