Latvia’s licensed non-bank lenders issued €1.003bn in new consumer loans in 2025. A separate business-purpose non-bank lending portfolio exceeded €1.1bn by year-end.

Latvia’s licensed non-bank lenders crossed the €1bn mark in new consumer lending in 2025.

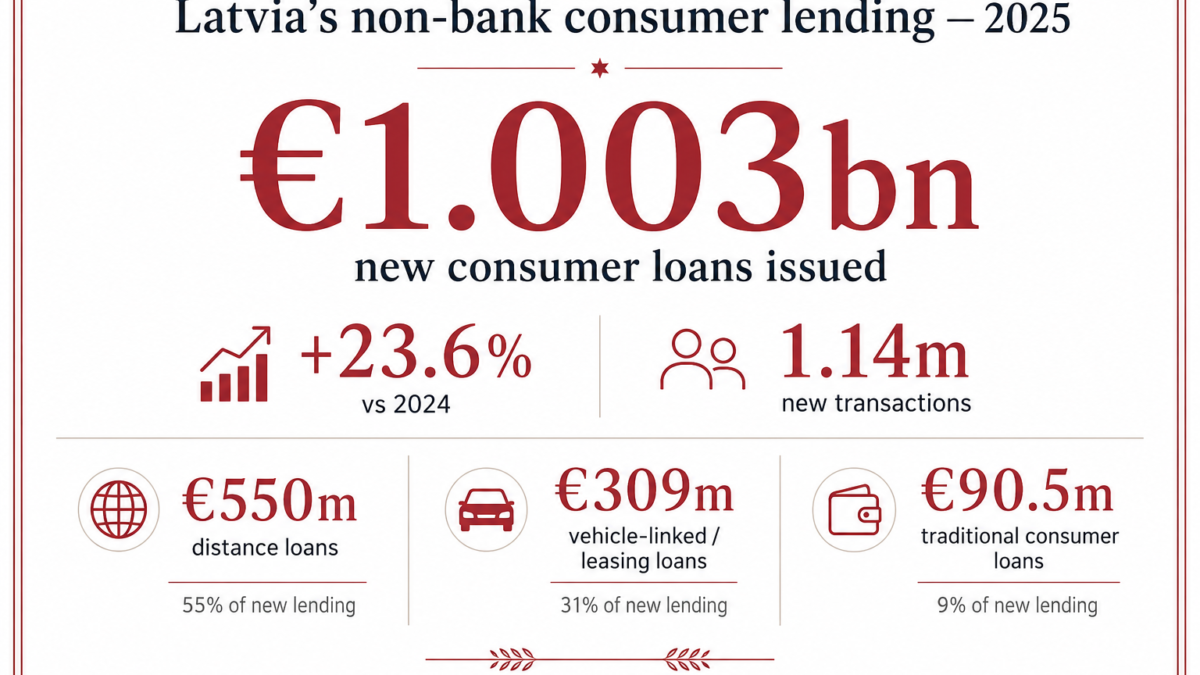

According to the Consumer Rights Protection Centre, they issued €1.003bn in new loans to consumers. That was 23.6% more than in 2024 — more than a fifth higher year-on-year. The number of new consumer-credit transactions reached 1.14 million.

Latvia’s non-bank credit market — 2025

| Indicator | Value |

|---|---|

| New consumer loans issued | €1.003bn |

| Year-on-year growth | +23.6% |

| New consumer-credit transactions | 1.14m |

| Consumer credit portfolio at year-end | €1.4bn |

| Business-purpose lending portfolio at year-end | €1.119bn |

Source: PTAC, review of Latvia’s non-bank consumer lending market in 2025.

The market is changing shape

The structure of the lending matters.

Distance loans were the largest segment, reaching €550m in 2025, or 55% of all new consumer non-bank lending. Their volume increased by 31.9% year-on-year.

Leasing and other loans secured by vehicles or similar objects formed the second major pillar, at €309m, or 31% of new lending. This segment also grew by almost 32%.

Traditional consumer loans moved in the opposite direction. New lending in this category fell to €90.5m, down 15.9% from 2024. Non-bank mortgage lending remained small, at €7.3m, while pawn-type loans against movable property reached €46.3m.

Part of the shift between consumer loans and distance loans should be read with caution. PTAC notes that the fall in consumer loans and the rise in distance loans were affected by one company’s change in data-reporting practice: after changes in loan application and approval channels, part of the volume was moved from the consumer-loan category to distance loans.

Even with that caveat, the direction is clear. The largest part of the consumer side is remote credit, while vehicle-linked finance has become the second major pillar. The old simple picture of the non-bank sector as a narrow short-term lending niche no longer captures the full structure of the market.

A separate business-finance layer

Consumer lending is only one side of the non-bank market.

In 2025, non-bank lenders issued €846m in new loans to legal entities and individuals for business purposes. The outstanding business-purpose portfolio reached €1.119bn at the end of the year.

Most of this portfolio was linked to leasing and other loans secured by vehicles or objects. That makes the non-bank sector relevant not only for household credit, but also for parts of business finance where vehicles, equipment and other secured assets are involved.

The banking sector remains much larger, but the comparison should stay methodological rather than dramatic. Bank loan books are stock measures, while PTAC’s €1.003bn figure is annual new issuance by non-bank consumer lenders. The point is not equivalence. The point is that the non-bank layer is now large enough to matter alongside the banking sector, not outside the credit system.

The next question is risk

The PTAC report does not show a simple deterioration story. By the end of 2025, 95.9% of the non-bank consumer credit portfolio, measured by volume, was either not overdue or overdue by up to 30 days. Loans overdue by more than 90 days accounted for a much smaller share of the portfolio.

But broader borrower-level data point to a different question. Kredītinformācijas birojs reported that by the end of March 2026, 702,000 individuals in Latvia had active credit obligations. Of those active borrowers, 152,000 — or 22% — had at least one loan overdue by more than 90 days.

That 22% is not a population-wide figure. It refers to people with active credit obligations in KIB data. The amount of credit obligations overdue by more than 90 days reached €986m, out of a total physical-person credit-obligation balance of €9.9bn.

These figures should not be merged mechanically with PTAC’s non-bank portfolio-quality data. They answer a different question: PTAC shows lender portfolio quality in one regulated segment; KIB shows borrower-level stress across a wider credit-information system.

For Latvia’s credit market, the €1bn threshold is therefore not just a growth marker. It is a reason to look more closely at how credit risk is distributed — between banks, non-bank lenders, non-financial arrears and borrowers who may appear manageable in one portfolio but stressed across several obligations.