Lithuania remains the strongest macro story in the Baltic region, but the June update from Lietuvos bankas makes the picture less simple than it looked in spring. The economy is still expected to grow, wages are projected to outpace prices, and the labour market remains favourable for workers. At the same time, the 2026 growth forecast has been revised down, exports are expected to contribute little, and part of this year’s demand will be supported by a temporary pension-liquidity effect.

Lietuvos bankas presents the current shock as less dangerous than the 2022 energy crisis. The argument rests on several buffers: lower dependence on imported energy and fossil fuels, stronger household balance sheets, earlier investment, productivity gains and a larger role for higher-value services. That is a credible resilience story, but it should not be read as immunity. Lithuania is better prepared than in 2022, not protected from the shock.

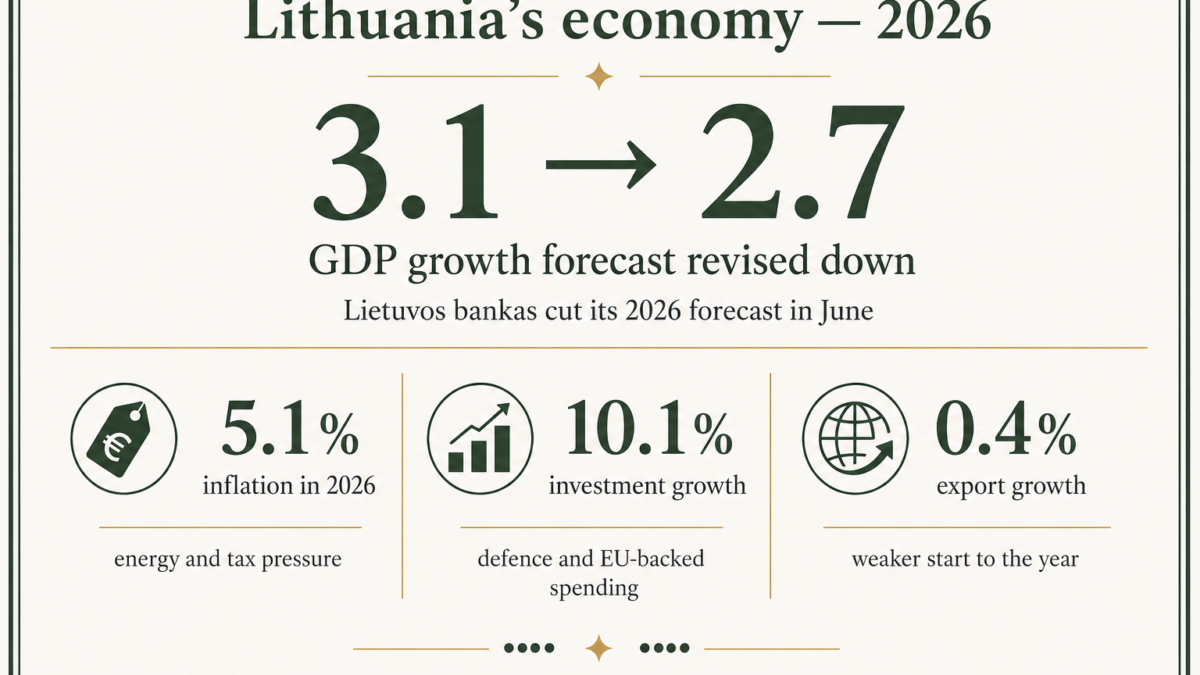

Data card: Lithuania — June 2026 forecast

GDP growth: 2.7% in 2026

Previous 2026 forecast: 3.1%

Inflation: 5.1% in 2026

Wage growth: 8.7% in 2026

Exports: +0.4% in 2026

Investment: +10.1% in 2026

The first important signal is the weaker start to the year. Lietuvos bankas cut its 2026 GDP growth forecast from 3.1% to 2.7%, explaining the revision by more modest first-quarter results rather than weaker fundamentals. That distinction matters. One quarter is not a trend, and it is too early to say that Lithuania’s export or services model has turned. But the beginning of the year does make the 2026 growth mix more fragile.

The second signal is the quality of growth. Lietuvos bankas expects exports to grow by only 0.4% in 2026, while investment is projected to rise by 10.1%. This means that the main impulse this year is not expected to come from a strong external trade position. It will come from domestic demand, public and defence-related investment, EU-funded projects, and the temporary boost from second-pillar pension withdrawals.

The pension effect is especially important. The new possibility to withdraw funds from the second pension pillar increases household disposable income and helps soften the impact of higher energy prices. But this is not a new source of wealth. It is a transfer of part of future savings into the present.

Data card: Pension liquidity as shock absorber

€2.06bn — left in bank and credit-union accounts

72% — share kept in accounts

€450m — withdrawn in cash

16% — cash share

€80m — early housing-loan repayment

€80m — early consumer and other loan repayment

This also explains why the pension effect should not be read as an immediate consumption boom. Most of the money paid out in April was still sitting in bank and credit-union accounts. But liquidity on household accounts can support spending gradually: some households may use it later for consumption, some may keep it as a precautionary buffer, and some have already used part of it to reduce debt. In all three cases, the effect helps the economy absorb the shock in 2026, but it is temporary. By 2027, Lietuvos bankas expects the positive impact of earlier withdrawals to fade.

Inflation is the third part of the story. Average annual inflation is projected at 5.1% in 2026, driven by higher energy prices, the Middle East conflict and tax effects. It should then decline to 3.0% in 2027 and 2.6% in 2028. The Lithuanian nuance is that inflation is not expected to erase wage growth. Average wages are projected to rise by 8.7% this year, 6.9% in 2027 and 7.2% in 2028.

This makes Lithuania different from a simple real-income squeeze story. Households may feel more cautious — Lietuvos bankas’ presentation shows weaker consumer sentiment even as household financial conditions remain relatively strong — but the central bank still expects real purchasing power to increase over the projection horizon.

There is also a stronger structural layer behind the resilience story. Lithuania’s services export base has expanded sharply over the past five years: Lietuvos bankas shows services exports rising by €11.8 billion, or 87%, between 2021 and 2025. This is why one weak start to the year should not be overread. Lithuania has built a broader services-export position, and that story has not disappeared.

Data card: Structural support from services

Services exports: +€11.8bn

Growth period: 2021–2025

Increase: +87%

Message: stronger high-value services base

Caution: 2026 export trend needs more data

The conclusion is therefore balanced. Lithuania is not entering 2026 from a position of weakness. It has stronger households, a broader services base, lower energy vulnerability and strong investment. But the 2026 growth story is less clean than the headline GDP number suggests. The economy is being cushioned by domestic demand, public investment, defence spending and pension liquidity, while export growth is expected to be almost flat.

The safest reading is this: Lithuania remains resilient, but 2026 is not yet proof of a new external growth cycle. It is a year in which earlier strength helps absorb a new energy shock. The real test will come later — when the pension-liquidity effect fades, export data for several quarters are available, and it becomes clearer whether the weaker start was temporary or part of a broader external slowdown.