The Baltic economies are expected to keep growing in 2026, but the regional baseline is no longer a straightforward rebound story.

The regional context is not neutral. Latvia, Lithuania and Estonia are small open EU economies, but they are also EU and NATO border economies next to Russia and Belarus. This does not turn every forecast line into a geopolitical story, but it does change the baseline: defence spending, energy security, infrastructure choices, investor risk perception and fiscal planning all carry a stronger security layer than in most of Europe.

Lithuania remains the strongest macro case, Estonia is moving back into growth, and Latvia’s banking system remains stable. Yet across the region, growth is being carried less by a clean export acceleration and more by domestic demand, public and defence spending, household buffers, credit conditions and fiscal choices.

The 2026 question is not whether the Baltics can still grow. It is whether this growth marks the start of a new investment and productivity cycle — or mainly shows how long existing buffers can absorb a more expensive environment.

Baltic baseline for 2026

Main signal: growth is returning, but the growth mix is uneven.

Lithuania

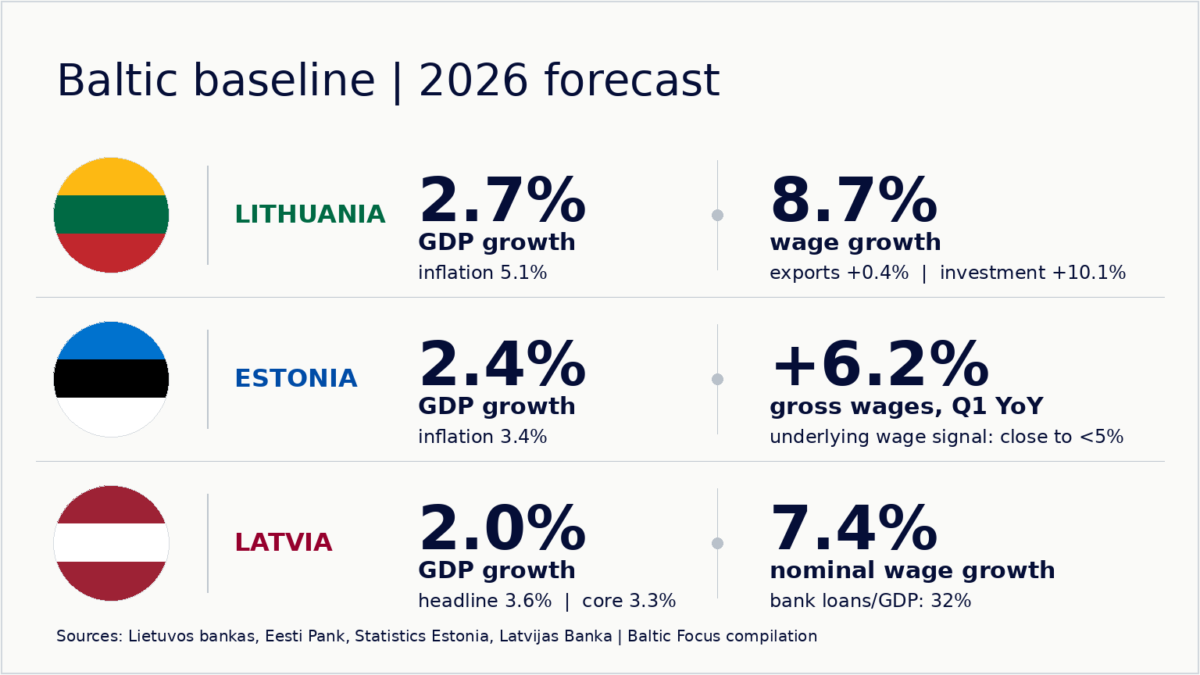

GDP growth: 2.7%

Inflation: 5.1%

Wage growth: 8.7%

Exports: +0.4%

Investment: +10.1%

Estonia

GDP growth: 2.4%

Inflation: 3.4%

Average gross wages: +6.2% YoY in Q1 2026

Underlying wage signal: close to but below 5% in the longer term

Main support: households and general government

Latvia

GDP growth: 2.0%

Headline inflation: 3.6%

Core inflation: 3.3%

Nominal gross wage growth: 7.4%

Bank loans to companies and households / GDP: 32%

The numbers already show three different baselines. Lithuania has the fastest GDP growth, at 2.7%, but also the highest inflation, at 5.1%, and almost flat export growth of 0.4%. Estonia’s growth forecast is close, at 2.4%, with lower inflation at 3.4%, but its recovery raises a funding-model question. Latvia grows more slowly, at 2.0%, while bank loans to companies and households still equal only 32% of GDP. This is not one Baltic cycle, but three recoveries with different constraints.

Lithuania: the strongest story is also less clean

Lithuania’s June update is less clean than the spring story, but it still leaves the country with the strongest headline forecast in the Baltic region. Lietuvos bankas revised its 2026 GDP forecast down from 3.1% to 2.7%, mainly because first-quarter results were more modest than expected. That does not prove a structural turn, but it makes the growth mix more fragile.

Even after the revision, Lithuania remains ahead of its neighbours in the headline numbers. Lietuvos bankas expects GDP to grow by 2.7% in 2026, wages by 8.7% and investment by 10.1%. The country also enters the year with stronger households, lower energy vulnerability than in 2022 and a broader services-export base. Higher defence spending adds a fiscal question to that resilience, but it does not remove Lithuania’s stronger 2026 starting position.

The quality of growth is the main issue. Exports are expected to grow by only 0.4% in 2026, while investment is projected to rise by 10.1%. This means that the main impulse is not expected to come from a strong external trade position. It will come from domestic demand, public and defence-related investment, EU-funded projects and the temporary boost from second-pillar pension withdrawals.

The pension effect is useful, but it should not be confused with a new growth engine. It increases disposable income and can support domestic demand in 2026, while the longer-term effects on consumption, savings and household balance sheets will become clearer only later. By 2027, Lietuvos bankas expects the positive impact of earlier withdrawals to fade.

For the regional comparison, the pension effect matters because it shows where part of Lithuania’s 2026 support comes from: household liquidity and domestic demand, not a stronger export cycle.

Lithuania therefore remains the strongest Baltic case in headline terms, but its 2026 growth mix is not clean. Wages, investment, public spending and temporary household liquidity support demand, while exports are projected to rise by only 0.4%. The open question is what replaces that temporary support in 2027.

Estonia: recovery returns, but the funding model is changing

Eesti Pank expects Estonia’s GDP to grow by 2.4% in 2026, supported mainly by stronger spending from households and the general government. After a weaker period, this puts Estonia back on a growth path, but the composition of that recovery matters.

The first structural issue is public debt. The problem is not Estonia’s current debt level, but the speed and direction of change. State debt was around €2.5bn in 2019, had grown to €10bn by 2025, and the Ministry of Finance estimates it could reach €20bn by 2030. Eesti Pank links this not only to fiscal discipline, but also to investment confidence. Companies are less likely to commit to long-term investment if future tax rises or spending cuts remain unclear.

The second issue is the funding model behind credit growth. Loans to domestic households and companies grew by 8% year on year in February, while deposits grew by just over 4%. The resident loan-to-deposit ratio has moved above one, and Eesti Pank’s conclusion is clear: local deposits are no longer sufficient to fund local lending.

This does not point to a current liquidity problem. It is a sensitivity signal. If domestic credit growth depends more on external and group funding, then market conditions, bond-market access and Nordic-Baltic banking-group priorities become more important for Estonia’s credit cycle.

Estonia’s credit growth therefore increasingly depends on a broader funding mix: intragroup funding, covered bonds, unsecured bonds and foreign deposits. Latvia and Lithuania are also part of that balance-sheet geography, both through non-resident deposits and through loans issued by Estonian banking groups in neighbouring markets.

The wage and income picture also needs to be read carefully. Statistics Estonia reported that average monthly gross wages reached €2,135 in the first quarter of 2026, up 6.2% year on year. Eesti Pank notes that if outlying figures are excluded, wage growth slowed from 6.3% in October and November to 5.3% in February and March, and that average wage growth should remain below but close to 5% in the longer term.

At the same time, tax changes strengthen the net-income channel. Estonia’s household support in 2026 therefore comes not only from gross wages, but also from tax-driven net-income effects.

For Estonia, the key signal is structure. The economy is recovering, but the recovery is running through a more complex financial system than before: rising public debt, faster credit than deposit growth, external funding, real estate exposure and regional banking links.

Latvia: stable banks, narrower core

Latvia’s 2026 Financial Stability Report shows a banking system that remains strong, but operates inside a narrower and still shallow financial structure. Latvijas Banka presents the sector as capitalised, liquid and resilient. At the end of 2025, the total capital ratio stood at 21.5%, CET1 at 19.2%, the leverage ratio at 9.0%, LCR at 206.7% and NSFR at 154.3%. The share of non-performing loans was 2.7%.

The structural question starts after those stability indicators. In 2025 Latvijas Banka revised the framework for identifying other systemically important institutions, or O-SII. After that revision, Latvia’s recognised systemic banking core became centred around Swedbank, SEB banka and Citadele banka, while Rietumu Banka and BluOr Bank were no longer identified as O-SII.

Latvijas Banka presents the O-SII revision as a methodological change. After that revision, Rietumu Banka and BluOr Bank were no longer identified as O-SII, while Latvia’s recognised systemic banking core became centred around Swedbank, SEB banka and Citadele banka. The practical consequences for credit intermediation, competition and borrower access will become clearer only later, especially towards the end of 2026.

In practice, this also means that a large part of systemic financial intermediation depends on institutions whose strategic decisions are shaped not only by the Latvian market, but also by wider Baltic and Nordic banking-group priorities.

Credit has revived, but from a low base. In March 2026, domestic loans to non-financial companies and households were up 11.8% year on year. Loans to companies grew by 13.3%, household loans by 10.3%, and housing loans by 9.7%. But bank loans to companies and households still stood at only 32% of GDP at the end of 2025.

That limits how much bank lending can support investment, housing supply and productivity growth. Latvia is not facing a visible banking failure scenario. It is facing a narrower financial structure operating inside an economy with shallow credit depth, scarce labour, persistent cost pressure and rising fiscal demands.

Inflation makes the story more uncomfortable. Latvijas Banka expects headline inflation at 3.6% in 2026, 3.8% in 2027 and 3.4% in 2028. Core inflation is expected to rise from 3.3% in 2026 to 4.0% in 2027 and 4.3% in 2028. That means the problem is not only imported energy. Services, wages, second-round effects and earlier cost pass-through remain part of the domestic inflation story.

Wages and inflation: household support, company pressure

Main signal: wages are still rising faster than prices, but this is not only good news.

Lithuania

Inflation: 5.1%

Wage growth: 8.7%

Reading: households remain supported, but inflation is high and export growth is weak.

Latvia

Headline inflation: 3.6%

Core inflation: 3.3%

Nominal gross wage growth: 7.4%

Reading: wages support income, but core inflation and labour costs remain part of the pressure.

Estonia

Inflation: 3.4%

Average gross wages: +6.2% YoY in Q1 2026

Underlying wage signal: close to but below 5% in the longer term

Reading: gross wage growth is more moderate than in Latvia and Lithuania, but tax changes strengthen net-income support.

The Baltic wage story is not a simple household-relief story. Wage growth helps purchasing power, especially where inflation does not erase it. But it also feeds company costs, services prices and competitiveness risks. In 2026, wages are both a buffer for households and a pressure point for the growth model.

Domestic demand carries the 2026 Baltic baseline

The 2026 Baltic baseline is more demand-supported than export-led.

Lithuania makes this most visible. Its economy is still expected to grow faster than its neighbours, but exports are projected to increase by only 0.4%. The stronger impulses come from investment, domestic demand, defence-related spending, EU-funded projects and pension liquidity.

Estonia’s recovery is also not described as a simple export rebound. Eesti Pank points to stronger household and government spending, while lasting growth will depend on whether companies invest, improve productivity and move towards higher value added.

Latvia’s growth is constrained by a different structure: stable banks, but shallow credit depth; labour shortages; sticky core inflation; and rising fiscal pressure. That makes a fast private investment cycle harder to assume.

Those external channels still matter. But in 2026 they do not carry the baseline alone. More of the growth burden is being carried internally.

What old advantages are no longer automatic?

The first old advantage is cheap or predictable energy. The region is less vulnerable than in 2022, especially Lithuania, but energy remains a live inflation and competitiveness channel. In 2026, energy still affects the Baltic growth model through company costs, household purchasing power and forecast risk.

The second is labour flexibility. The Baltics cannot simply release pressure through unemployment, wage cuts or emigration without damaging the growth base. Labour shortages are structural, wage growth remains strong, and demographic limits are part of the economic constraint.

The third is fiscal room. Estonia still has low debt by European standards, but the direction has changed. Latvia faces rising policy pressure, with defence and public investment competing for space. Lithuania’s public and defence-related investment supports growth, but also becomes part of the fiscal equation.

The fourth is simple credit expansion. Estonia shows that credit growth can require a broader external and regional funding mix. Latvia shows that a resilient banking sector can still operate in a shallow-credit economy. Lithuania shows that household liquidity can cushion demand, but temporary liquidity is not the same as a permanent engine.

The fifth is the assumption that export growth will automatically pull the region forward. In 2026, that assumption is too weak. Lithuania’s export growth is almost flat in the forecast. Estonia’s recovery needs productivity and investment to become lasting. Latvia’s structure limits how much domestic credit can support a stronger private investment cycle.

Conclusion: buffers are not a growth model

The 2026 Baltic baseline combines growth with a more demanding structure behind it. Domestic demand, public spending, defence investment, household buffers and credit conditions are carrying more of the regional story than a clean export acceleration.

This makes 2026 a test of the next Baltic growth model: whether resilience can turn into investment, productivity and exports, or whether the region is mainly absorbing a more expensive environment.

Cheap energy cannot be assumed. Labour is scarcer. Fiscal room is tighter. Defence spending is now part of the macroeconomic equation. Credit is recovering, but the banking and funding structures behind it are more concentrated, more regional and more exposed to market conditions. Export growth remains important, but it is not carrying the 2026 story on its own.

In that sense, 2026 is not only a recovery year. It is a transition year. The Baltics still have buffers: stronger households and services capacity in Lithuania, recovering demand and tax-supported incomes in Estonia, and resilient banks in Latvia. But buffers are not the same as a new growth engine.

The regional question is whether Latvia, Lithuania and Estonia can turn resilience into a new investment, productivity and export cycle — or whether 2026 will mainly show how well the Baltics can absorb shocks without yet proving that they have built the next model.

Sources: Lietuvos bankas, Eesti Pank, Statistics Estonia, Latvijas Banka, Latvia’s Financial Stability Report 2026.